The luxury fashion industry spent the entirety of the 2010s educating customers, shepherding them into pastures of elevated taste and high price tags. Brands opened doors to become (slightly) more inclusive, and designers became as popular as pop stars or sports teams. For affluent shoppers, new worlds of possibilities opened: a hoodie could cost $1,000, jeans could be made of leather, you could dress like Jeff Goldblum if you really wanted to. Those who couldn’t afford the mainline could buy a downmarket collaboration – or a dupe.

As trite as it may sound, fashion is a form of self-expression, whether you’re Jeff Goldblum or anybody else – self-expression for the wearer, along with the person making the clothes. In theory, all of the channels that connect those two dots, from conceiving a collection to snapping a mirror selfie, should serve that goal. Needless to say, that isn’t always the case.

Luxury fashion’s efforts to go mainstream worked. But the shoppers and fans who spent that decade consuming, learning, and evolving began to feel disenchanted by the luxury promise. It was a classic case of the student becoming the master. Luxury brands couldn’t consistently deliver the ingenuity and craft these savvy new buyers expected, and when they did, it came at an exorbitant price.

That’s what led to the creation of this White Paper, based on a survey of more than 6,000 luxury consumers and made in collaboration with Boston Consulting Group. Luxury shoppers are smarter than ever, and they expect the brands they buy to be as smart as they are – if not smarter. They see the ways fast fashion is mimicking luxury, and vice-versa. The crisis the industry is facing isn’t about demand for nice things; it’s about a growing aversion to outmoded ideas of marketing and selling those things.

The opportunity now is for independent designers and the consumers who love them to thrive. We don’t want to buy things that feel like they were dreamed up in a conference room, and we don’t want to buy from a brand constantly jumping from new gimmick to new gimmick, trying to satisfy everyone, never landing on a consistent idea with depth and durability. Even brands that aren’t independent can and must start acting like they are.

For years now, Highsnobiety White Papers (made in collaboration with Boston Consulting Group) have tracked and analyzed our readers’ obsessions and perceptions alongside consumer behaviors at large. We’ve made it our business to know what’s happening in fashion now and who might best guess what’s next.

In 2019, we analyzed the zeitgeist we deemed The New Luxury. At that time, our readers specifically expressed interest in retail as art practice, with access for the first in line, in the form of limited editions, tipped-off drops, and unexpected collaborations. Brands were smart to emphasize the experiential, making luxury conceptual, earnable, and exclusive via hyper-awareness.

In 2020, we asserted that to succeed in an oncoming environmental shift, brands wouldn’t “simply respond to trends or outside narratives, but instead become true drivers of culture.” They would emphasize “building scenes, developing stories, and enabling access to a moral and aesthetic universe, [because] cultural credibility is more than just an idea in abstraction, but a set of quantifiable brand and product attributes.”

Within the entirely different markets and headspaces of 2025, we’re looking back at these and other studies while examining what has changed and what has stayed the same. Anecdotally, brands with more consistent storytelling, be they young or centuries old, are in. Novelty acts such as the aforementioned artist collabs and limited drops, less so.

This rejection of anything that may be considered a stunt speaks to, we believe, a reactive desire for stability and authenticity. Six years ago, we predicted that the future of luxury fashion branding was cultural credibility. Today, we see, through the lenses of research and instinct, that this is now firmly the case.

The next generation is over the hype. Instead, they crave connection. Brands that can evolve thrive, while those that don’t skirt irrelevance.

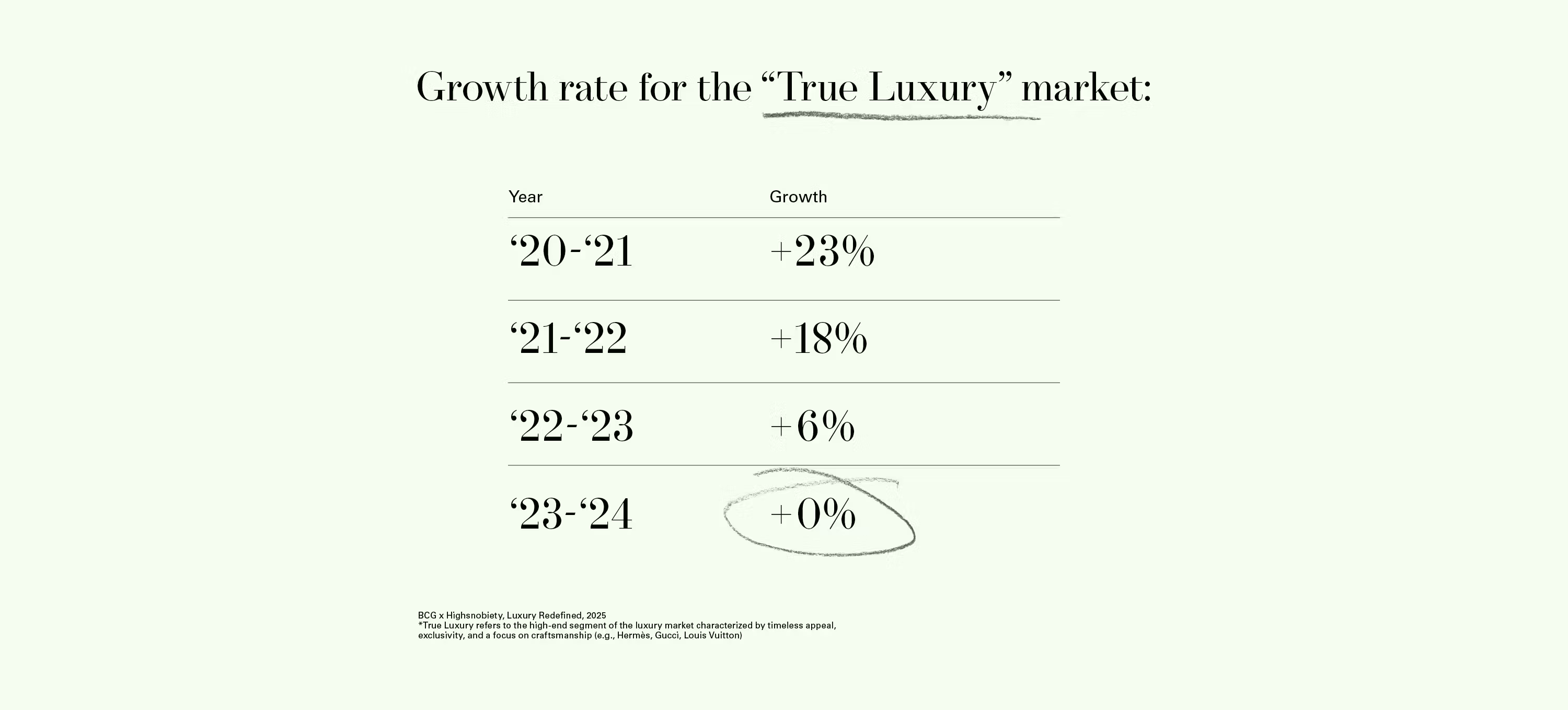

According to analysts, the luxury sector is flailing, losing ground with loyalists and prospective customers alike. This news served to guide our next set of White Paper questions: What do luxury consumers want their favorite brands to do differently? And maybe more importantly, are we living in a time of post- or peak-luxury?

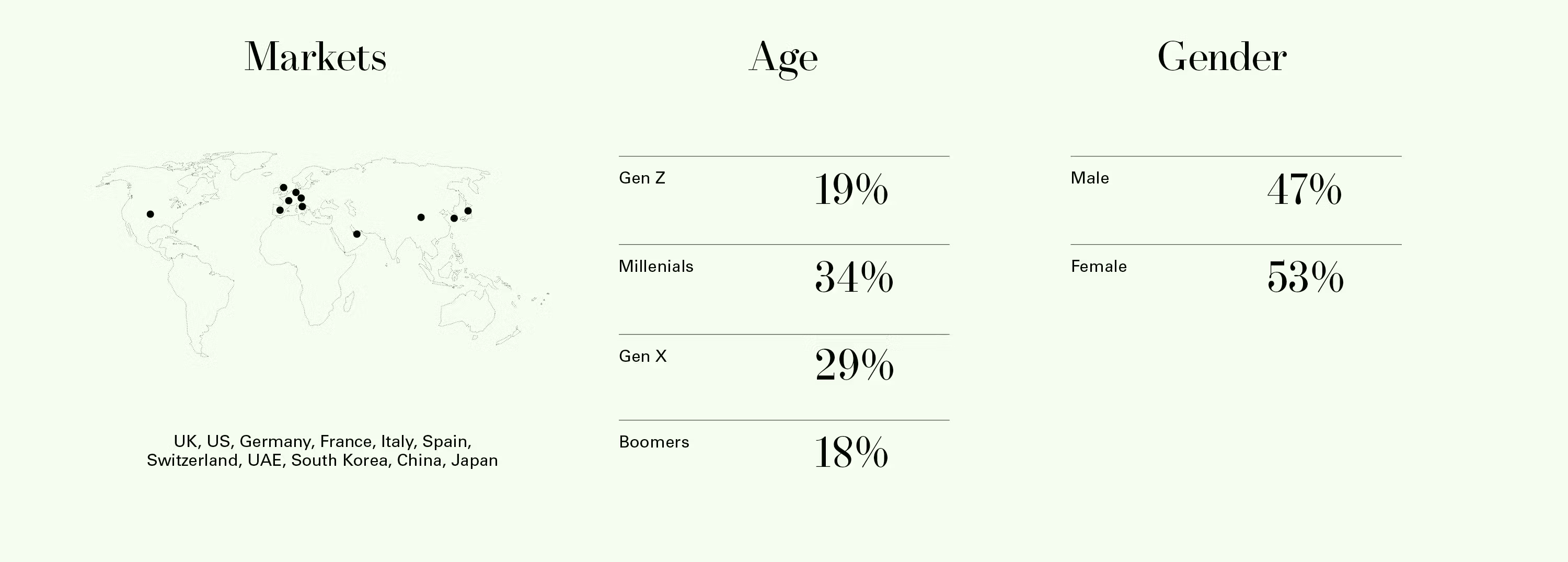

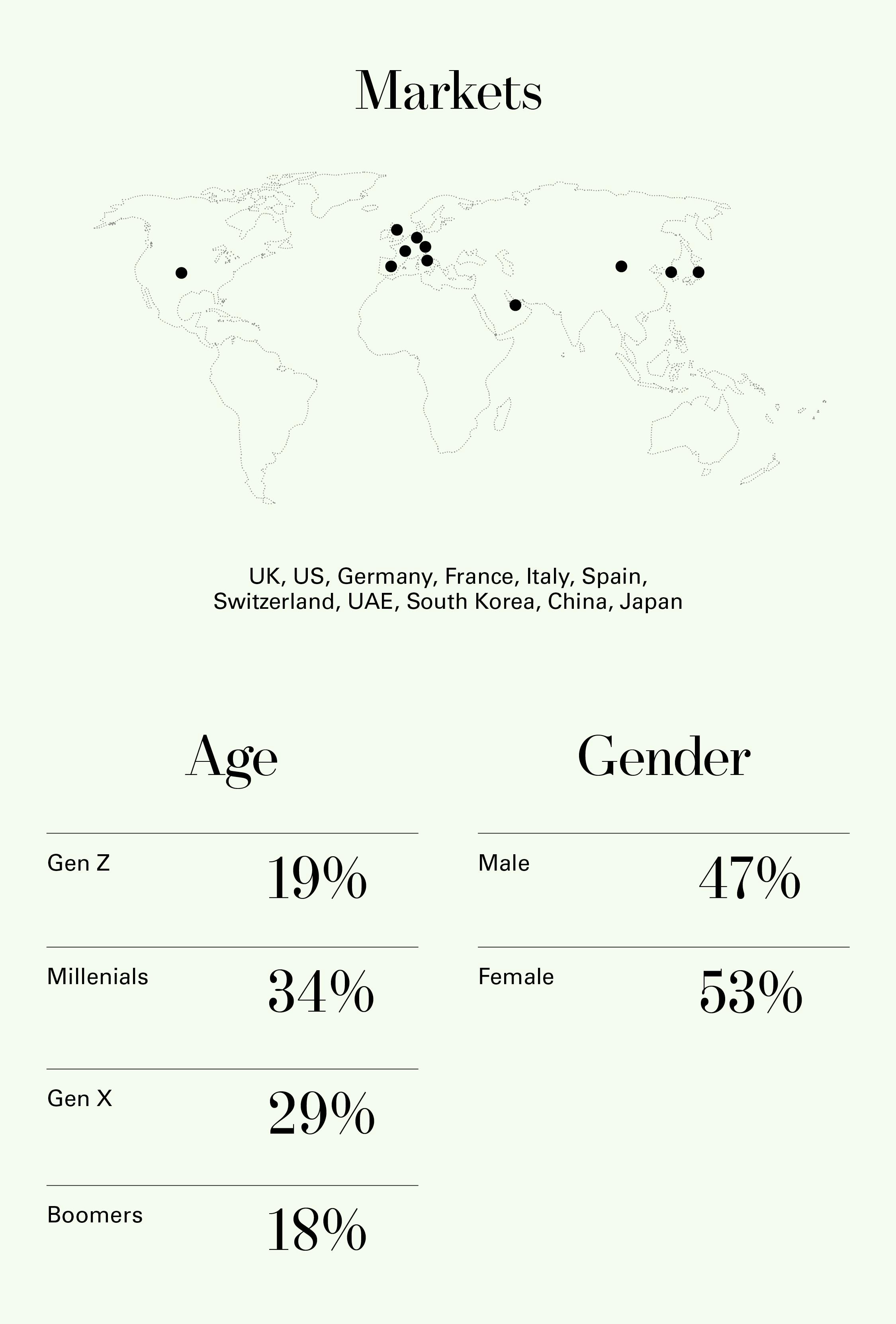

We conducted a survey in partnership with Boston Consulting Group. Our largest yet, it interviewed 6,710 respondents across 11 key markets: China, South Korea, Japan, the US, the UK, Spain, France, Italy, Switzerland, Germany, and the UAE.

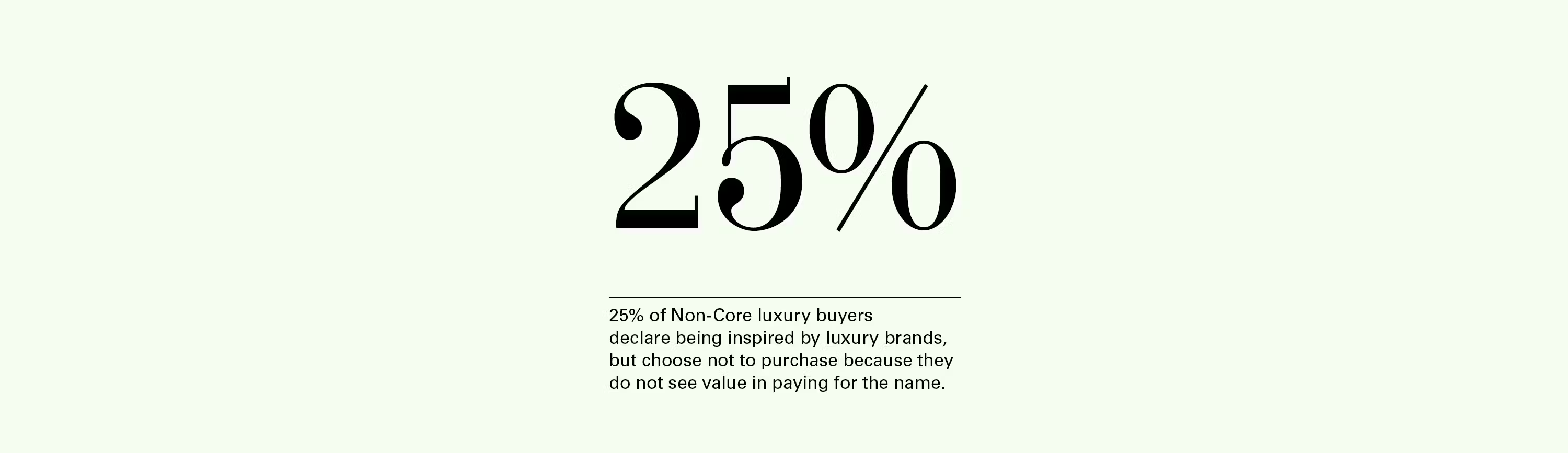

For precision on certain queries, our respondents were sectioned into Core and Non-core Luxury Consumers based on their reported 2024 spending patterns. Core Consumers, who spent over €10,000 (or the equivalent) on luxury items including classic heritage brands (Chanel, Louis Vuitton, Cartier, Dior, Burberry) as well as independent, new, or niche brands, made up 70% of our survey.

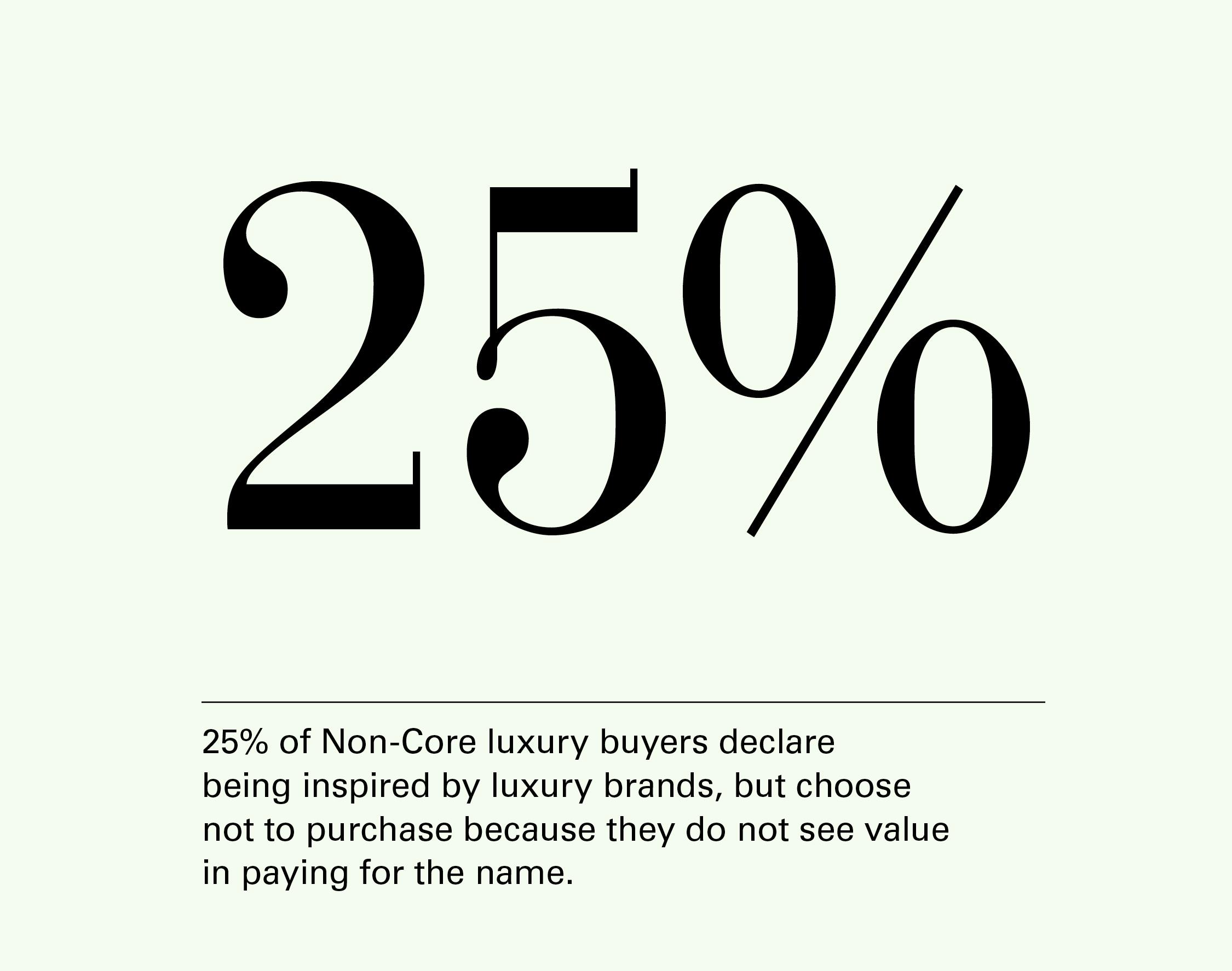

The remaining set, while they could ostensibly afford to spend as much on luxury fashion, decided against it. A high percentage of this group (25% overall) said that, while they were inspired by it, they did not see the value in paying for the names of classic luxury brands.

We combined BCG’s extensive research with our own internal polling, which involved industry experts and consumers with exacting tastes, also from around the world. Much of what we saw and heard was in line with our own thinking: that a higher importance is being placed on brands’ cultural fluency. Fashion fans have grown suspicious of gimmick, overvaluing, and diminishing material quality. They want their clothes to catch up – to be and feel as smart as they’ve become.

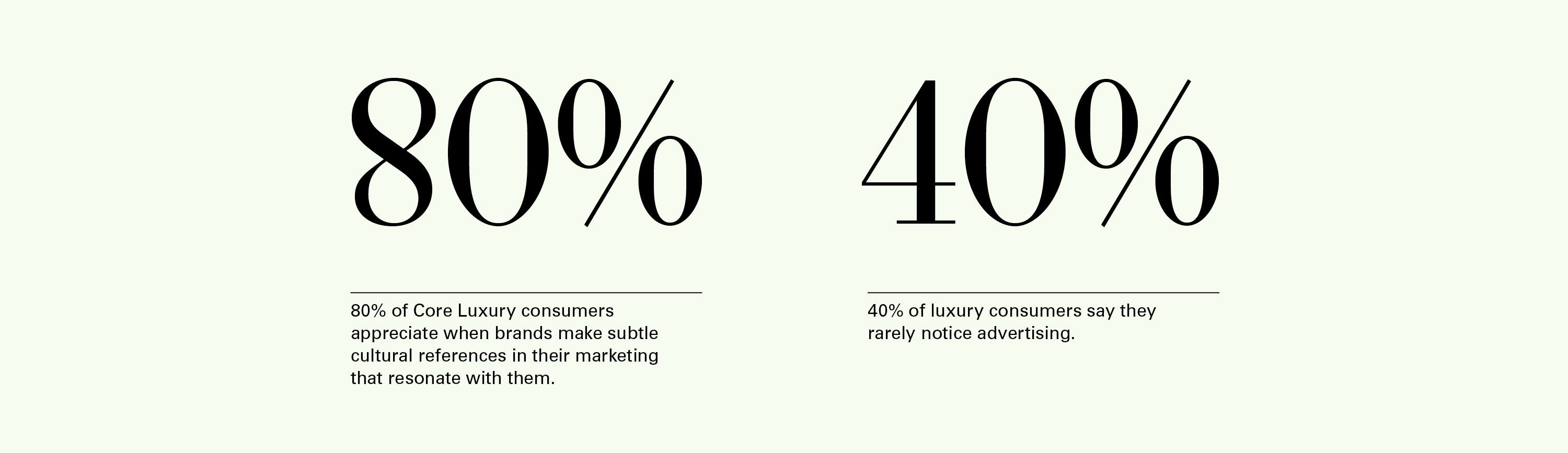

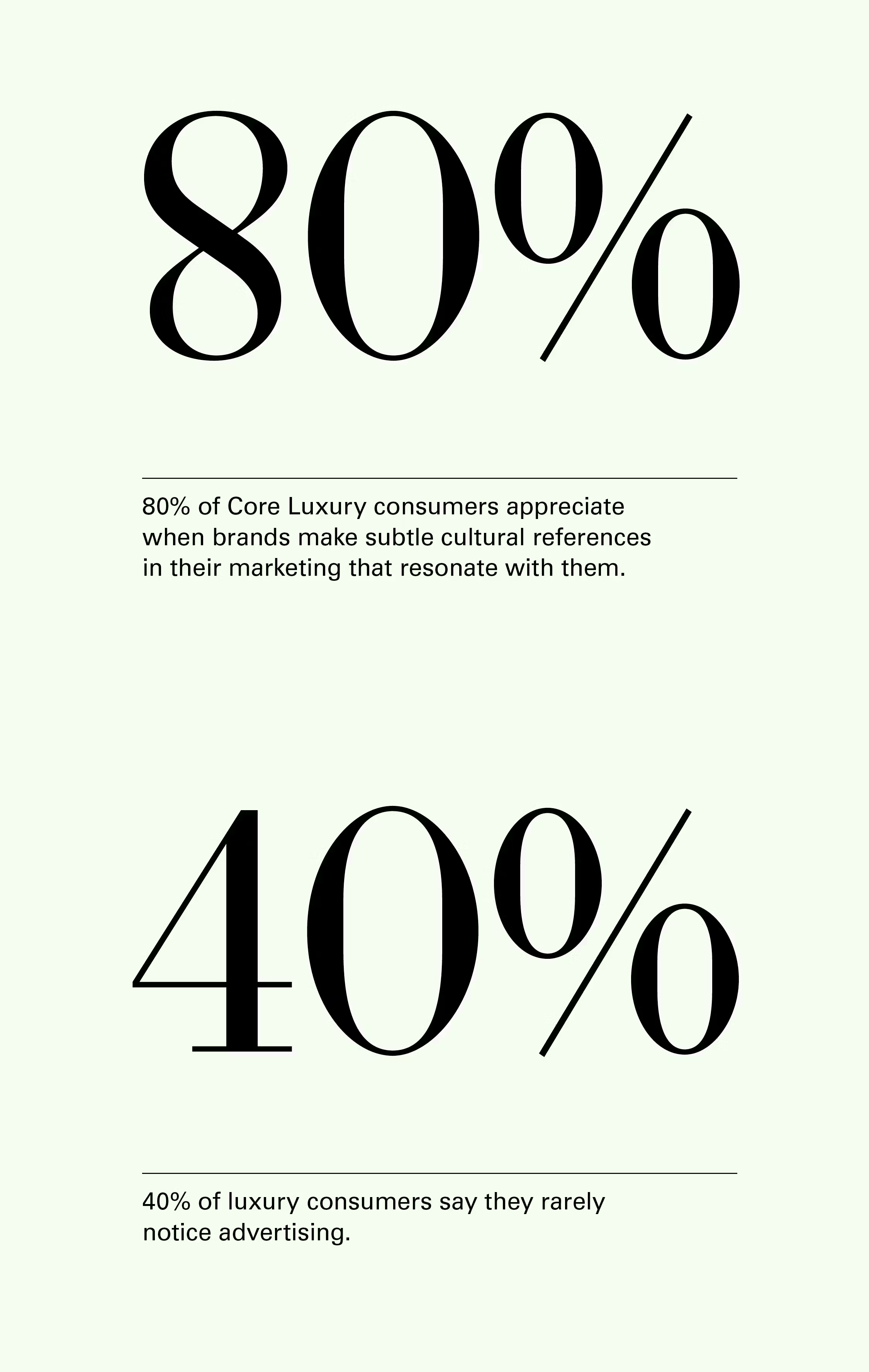

Eighty percent of Core Luxury respondents said they agree with the statement, “I appreciate when brands make subtle cultural references in their marketing that resonate with me.”

This stat may at first appear insignificant or a given, but that a large majority of our key demo, spread over continents, genders, and generations, feels that brands would be smart to level with them is in fact extremely revealing of today’s landscape.

Discovering motivations behind purchasing patterns is never easy. Consumers – as we all know, being consumers ourselves – can never fully explain the true nature of their own shopping behaviors. When this many people align on a statement this detailed, we pay attention. It tells us that luxury shoppers are satisfied to be treated with care and intelligence, to be seen as who they are and met where they are – that the world has drastically changed, and yet luxury marketing for the most part hasn’t.

Core Luxury Consumers will, in short, buy into brands that get them – that speak to instead of talking at them. In a micro sense, this means mix-and-match pieces that allow for seamless wardrobe integration. On a macro level, we see this stat as a call for brands to stop dictating and start resonating, to ditch the larger-than-life logos and focus on craft.

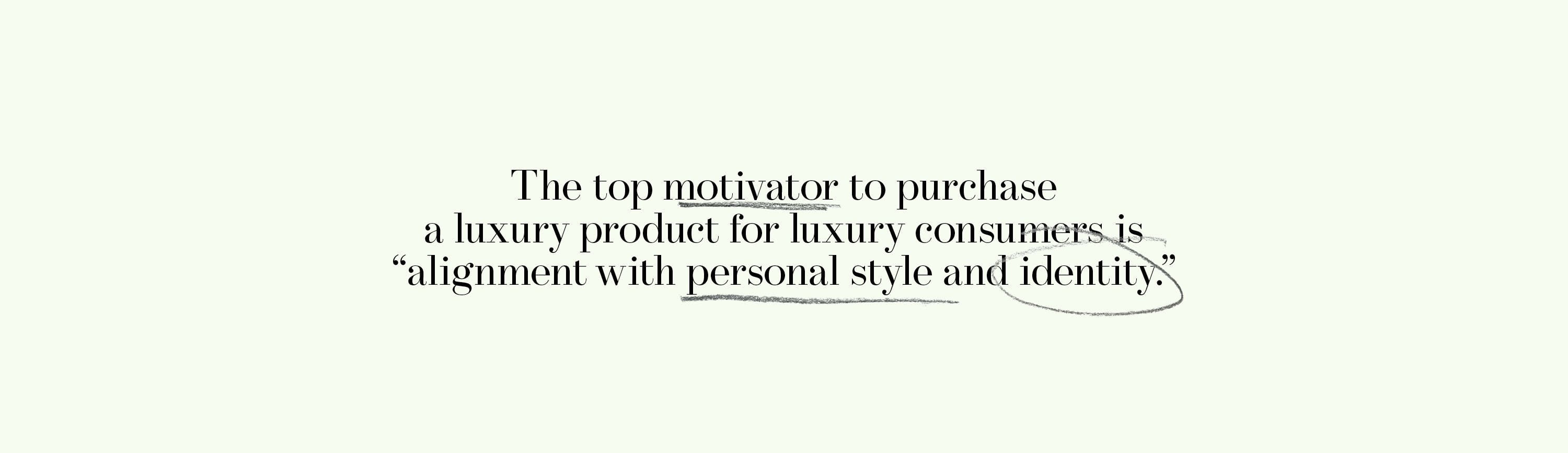

As opposed to being shown brand worlds into which they’re expected to fit, consumers want products that will fit into their lives as is. Further proof of this: The top motivator to purchase a luxury product for Core and Non-core audiences is “alignment with personal style and identity.”

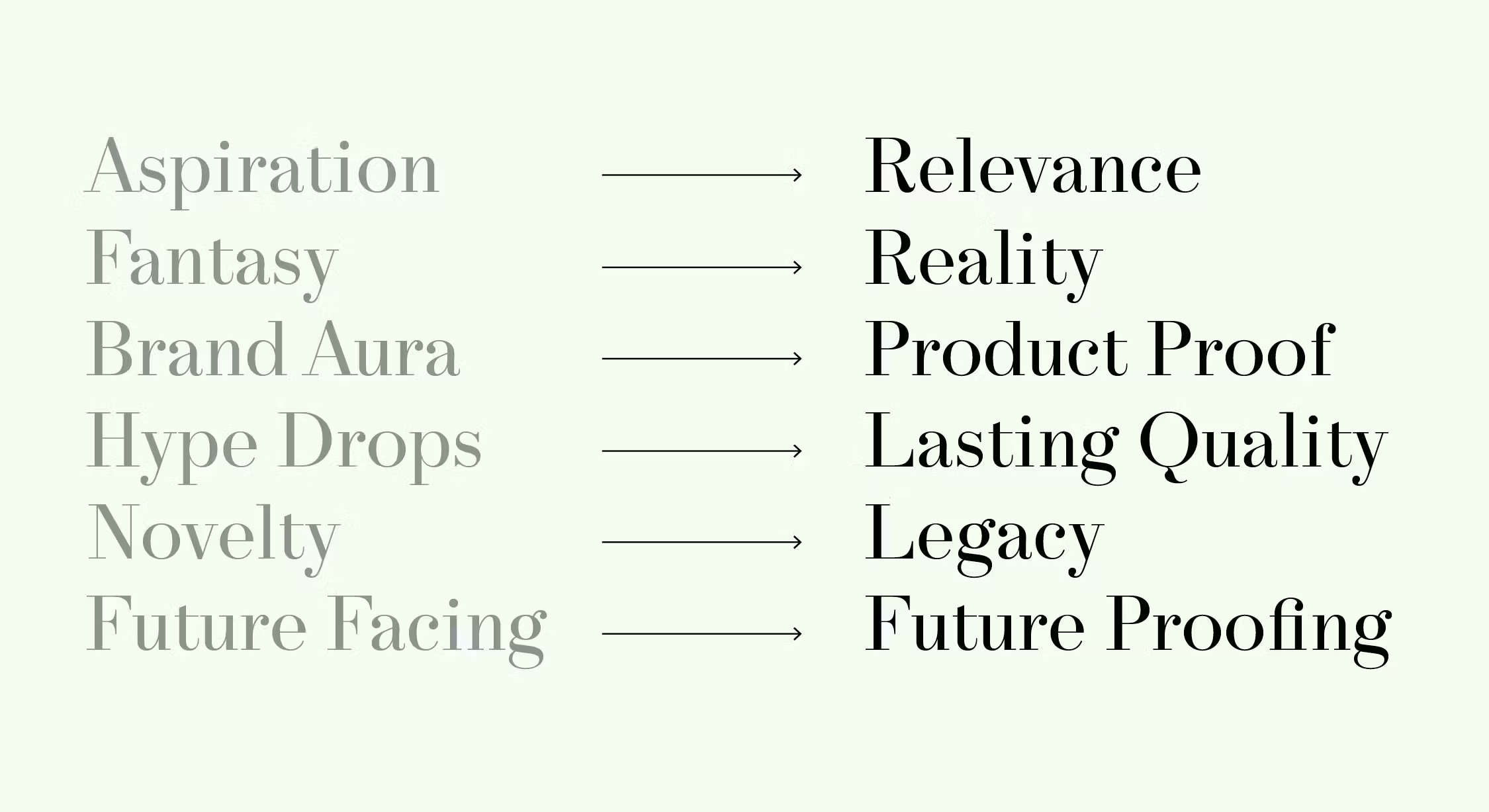

If most consumers say luxury is not what it used to be, they’re not rejecting luxury itself – they’re rejecting outdated ideas.

Today’s fashion reportage is working up a lather about a luxury crisis. It started with the retail apocalypse, during which department stores and online boutiques with expensive buys were unable to compete with Amazon and DTC sales, and headed into a global pandemic that shuttered more shops and caused distribution fiascos.

Which leads us up to 2025, when top-earning heritage brands are reporting losses – this, arguably due to yet another flaw in the fashion system: inevitable homogenization, after years of unchecked licensing and conglomerate-owned brands sharing resources, including strategies.

We’ll get to other factors and findings that will give us more insight on that, but first let’s look at the phrase “luxury crisis” from another angle. Luxury itself cannot, by definition, be in crisis. That is, a state of extravagance can either be or not.

We are not, to be clear, in danger of seeing ideas of luxuriance (from over-the-top decadence to purified steam) cease to exist. The word luxury, here, is synecdochal, a large concept standing in for a narrow one: the high fashion industry. The word crisis, too, is hyperbolic: Even the complete absence of luxury/fashion would not be a disaster. In fact, luxury crisis is an oxymoron, made of contradictory terms but meaningful all the same.

This is a matter of semantics, but when we hear these words placed together, we tend to evaluate our own affiliations, asking what luxuries we include in our lives, which aspirations are still out there, what feels less enticing than before, where and how much money was spent, and whether the product is worth the price.

Indicators of luxury are consistently ripped off downmarket and sold en masse at lower prices – either as illegal fakes or legal duplicates, the mood board of which is easily guessed. We see this from year to year, season to season, and even day to day with viral products and their copycats. Trademarked signatures such as logos and the red bottoms on Christian Louboutin shoes attempt to gum up the works of this vicious cycle, at least offering legal protection of certain designs.

And yet by now, we’re all more than used to a “look for less” proposal from fast fashion. Recently, the lower tier (which usually has higher earnings) is investing in mimicking the environs of their influences as well. Anecdotal evidence of this was offered by the style newsletter Blackbird Spyplane in February 2025, via a side-by-side showing a Zara men’s suiting section and Evan Kinori’s almost identically set-up studio.

As ever, when the symbols of better living become ubiquitous, they inherently hold less cachet. A new definition of luxury must surface. But as technology such as artificially rendered imagery and reactive computational designs further speed up this cycle, a breaking point is bound to be reached. Fashion is prone to get so fast; the only response is to slow down.

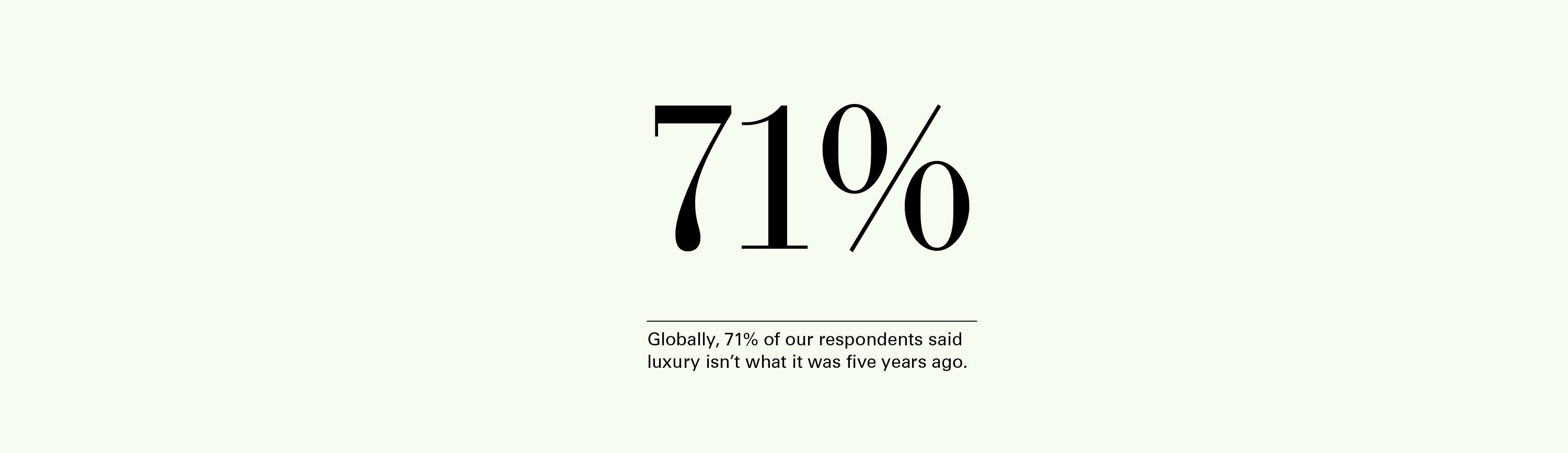

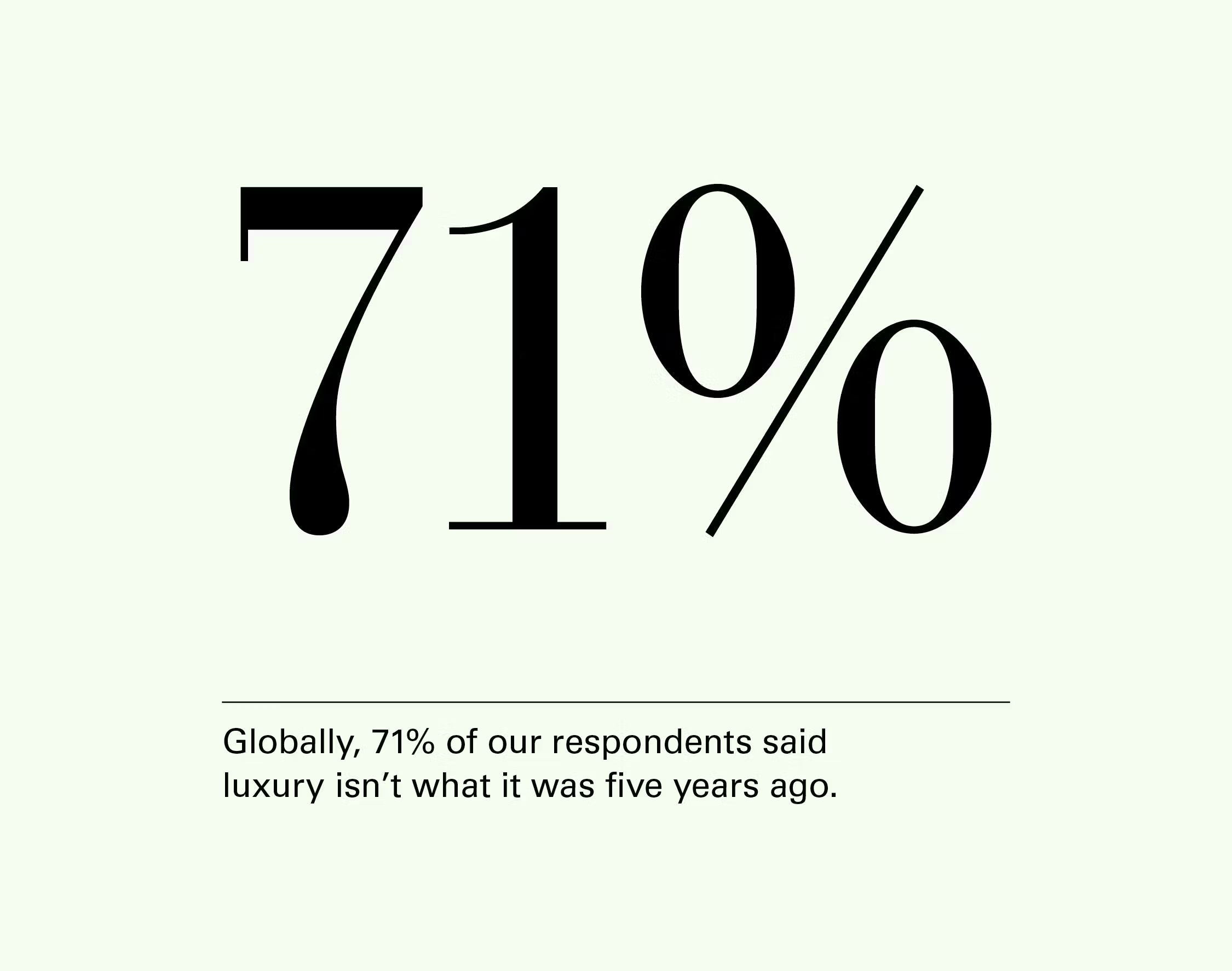

The survey question above (“Is luxury fashion what it was five years ago?”) pertains to a blurring of the line between high- and low-end. As prices rise and offers feel less distinguishable from one another, potential purchasers are less certain about the inherent value of a label.

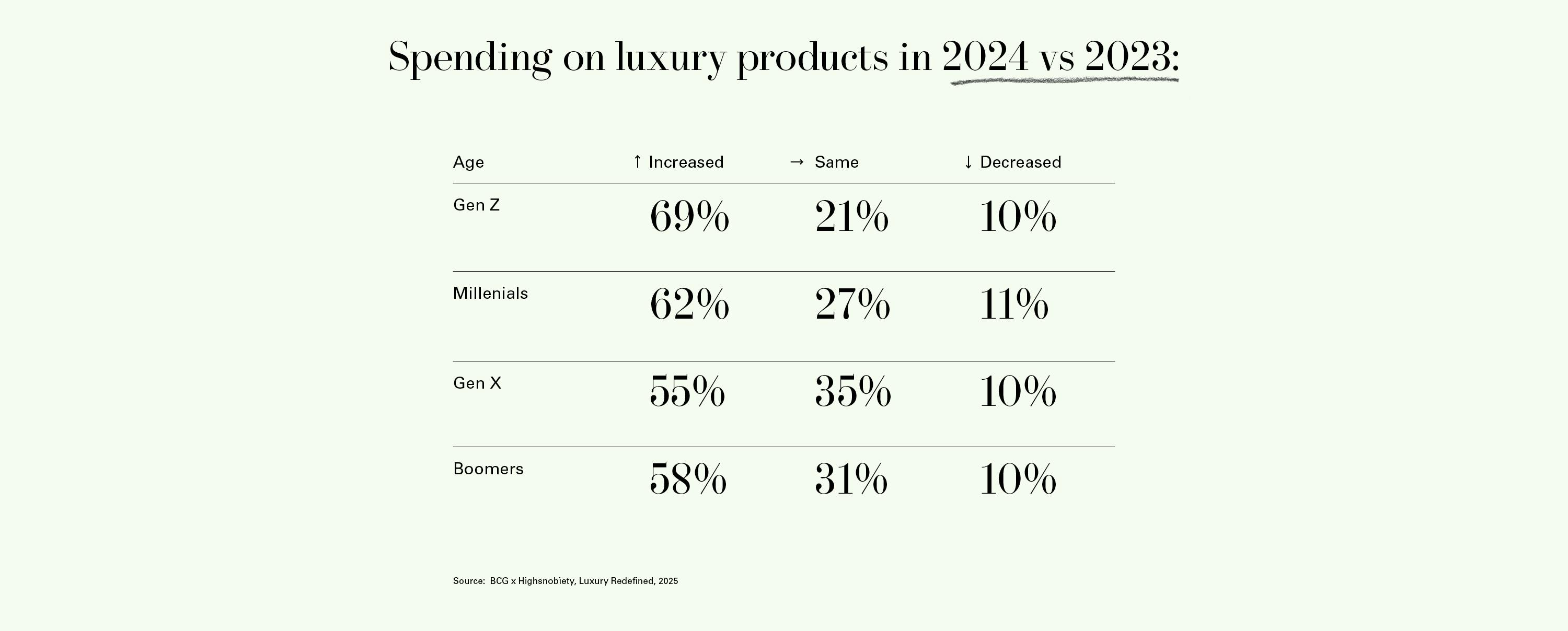

Luxury consumers are spending as much as ever, especially younger ones. To the question of how the amount they spent on luxury products in 2023 changed in 2024, the largest percentage of respondents (from each generation, in every market, across genders) answered that their spending increased. The smallest percentage of respondents answered that it decreased (with more saying it stayed the same).

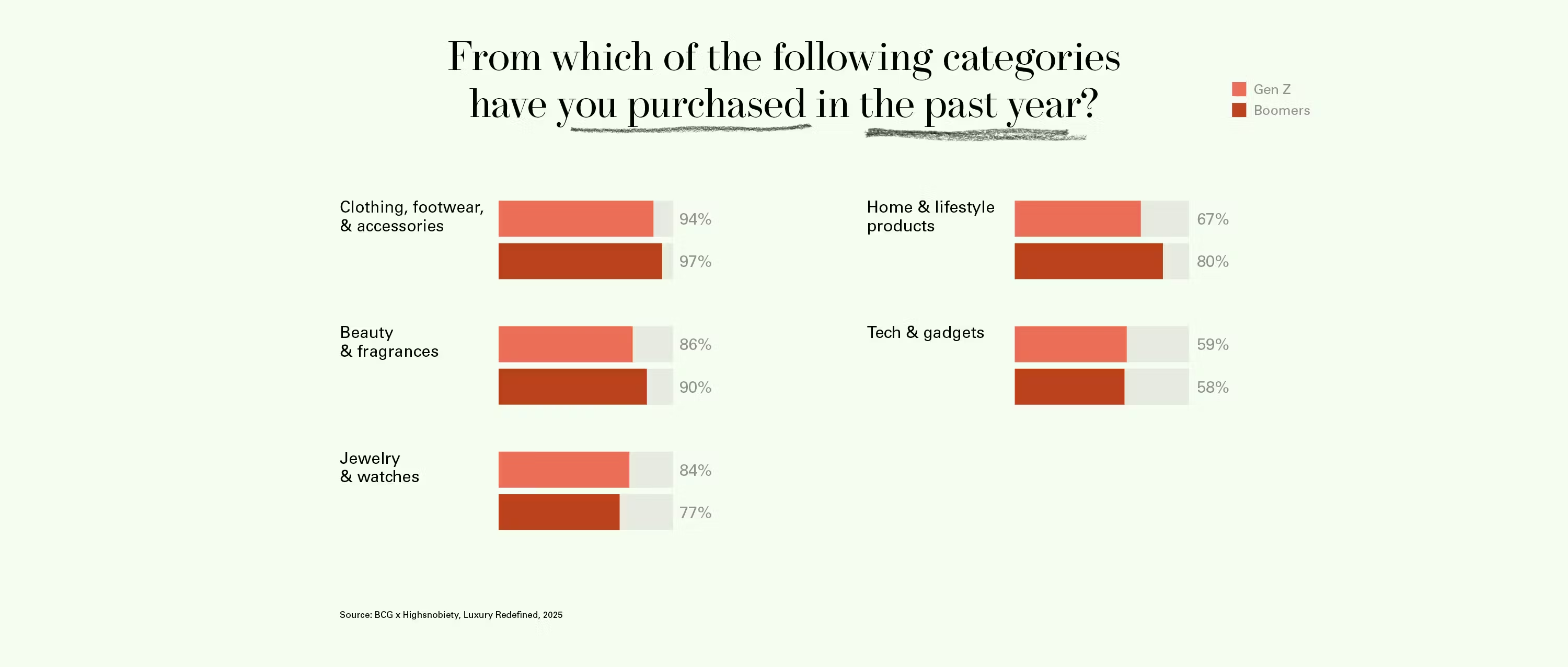

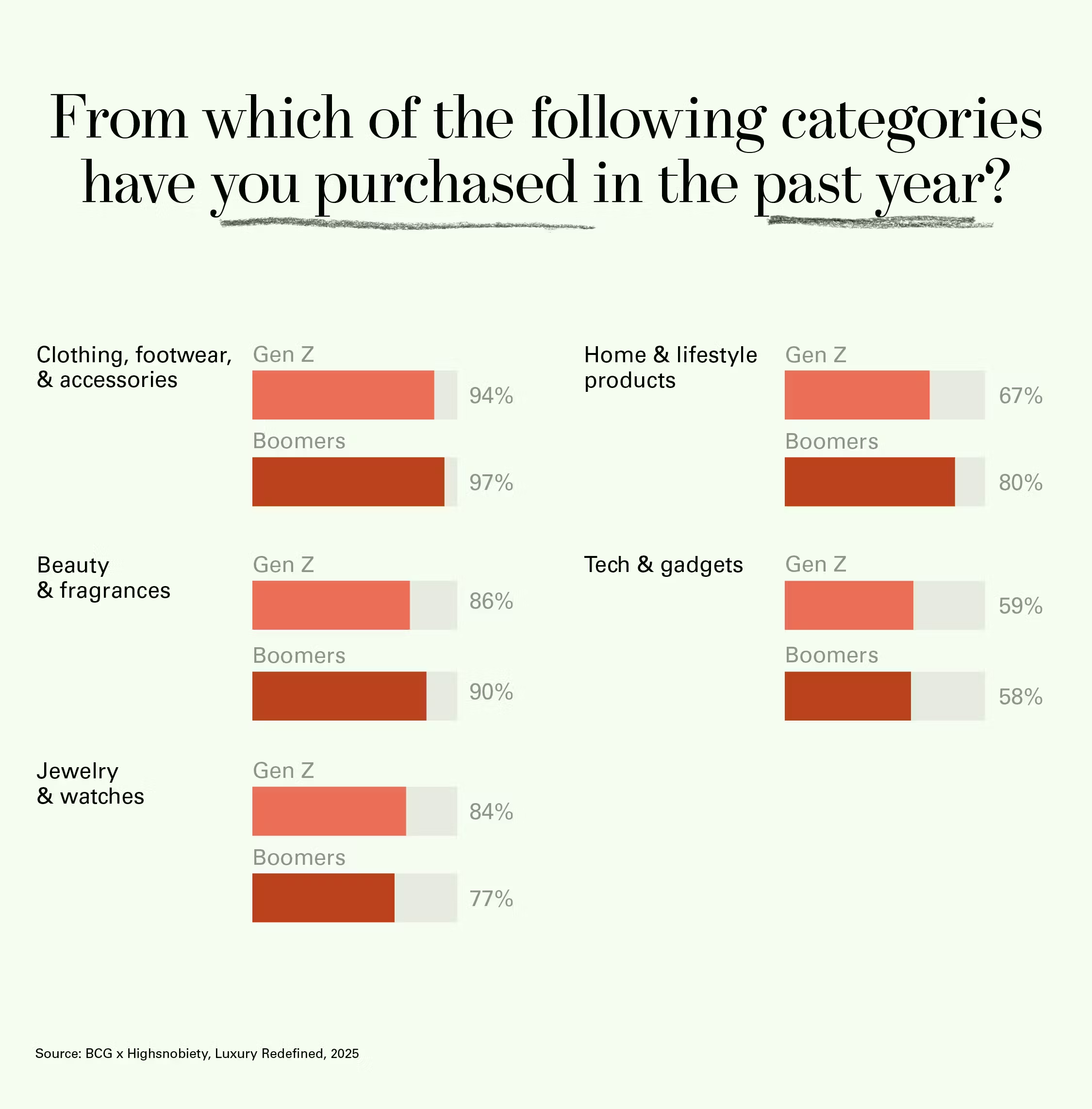

The younger set are even investing almost as much in non-fashion purchases, such as homeware and beauty products, as they are in clothing, shoes, bags, and sunglasses. In fact, our survey shows that Gen Z and millennials are more likely to buy jewelry and watches than their Gen X and boomer counterparts.

When Kate Bush’s 1985 track “Running Up That Hill” became the most-streamed song on UK and US Spotify in 2022, it also broke the record for longest gap between single release and number one chart status in the UK, underlining a pivot already in progress: With access to almost anything from any era at our disposal, newness now holds less of an edge.

This much-discussed music phenomenon begs a question applicable to culture industries writ large: Why would the top item of any given year necessarily be something produced during that year (as it almost always is)? The answer: Newness, or affiliation with a moment, used to count for quite a lot. The novelty of a trend being from now was enough to elevate its better aspects to a higher status, for the time being.

The desire to keep up with these cycles, to interpret the best of the new, propels the consumer, the designer, the producer, and the retailer. It has defined our modern understanding of fashion for centuries. So, what happens when, from the recesses of our tailored advertisement feeds, the excitement of constant refreshing wears off? What does the world of fashion look like when quick reactivity is valued less?

Within our lifetimes, new has become synonymous in many ways with worse: made cheaply, reactively, perhaps with AI, and limited creatively by the demands of a global market. Laments of nothing ever really being new, anyway (such as in the film industry: it’s all remakes, sequels, rehashes, retro), and of algorithm fatigue hindering a sense of discovery make that quest for a hot take feel ever more beside the point.

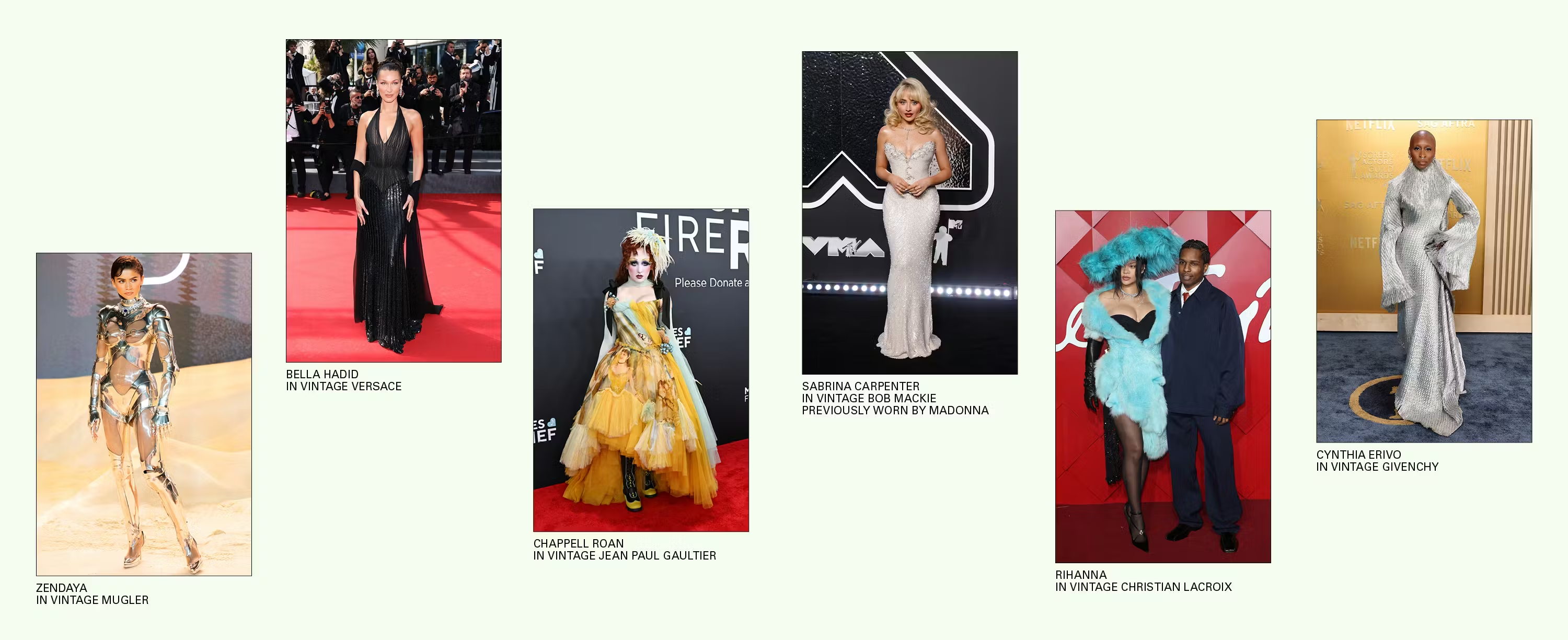

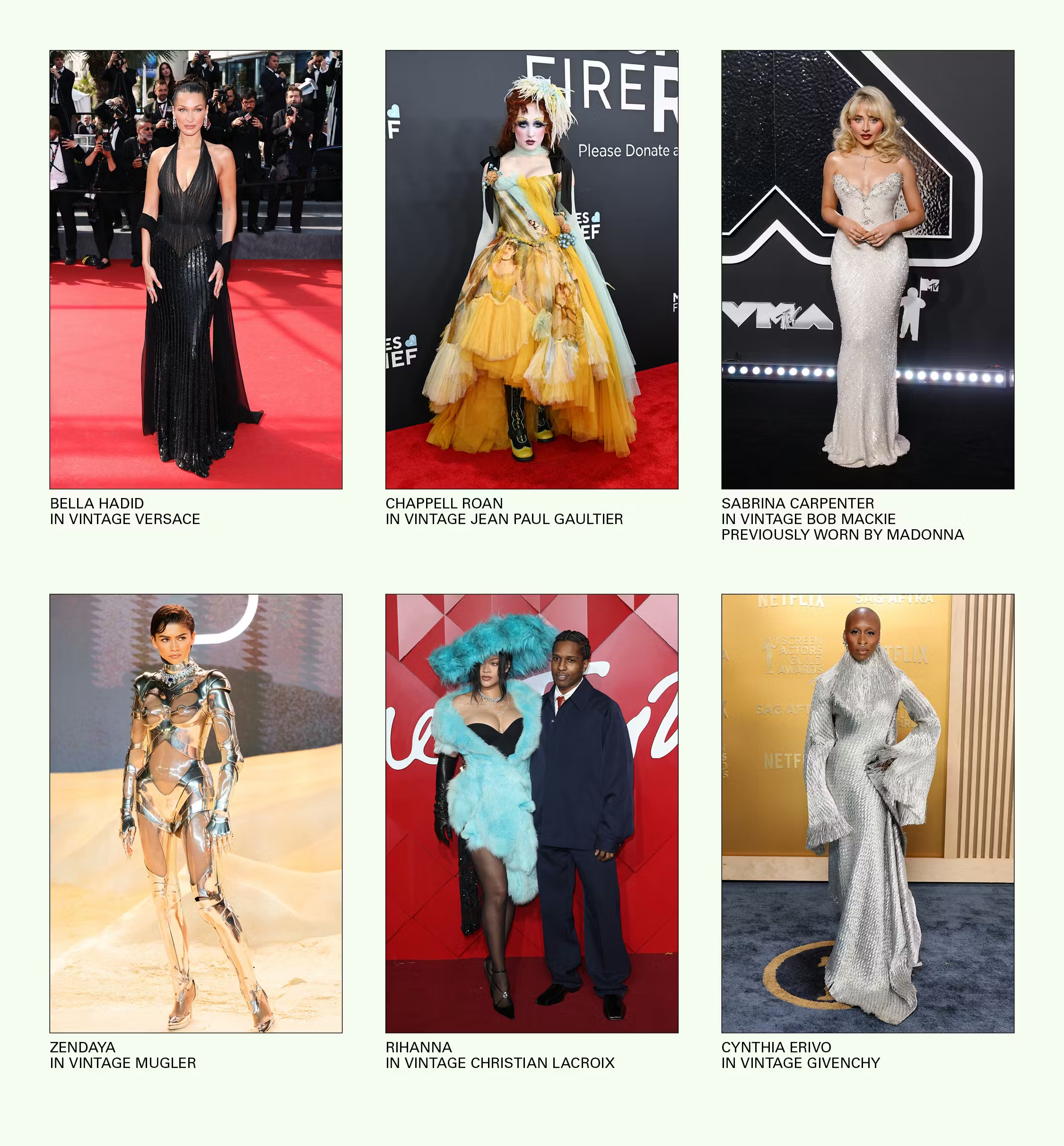

The old becomes new, as with a proliferation of vintage pieces on red carpets. Celebrities are opting for designs of the deceased – Roberto Cavalli, Paco Rabanne, Vivienne Westwood, Thierry Mugler – the retired – Jean Paul Gaultier, Tom Ford, Bob Mackie – and especially the almost-cancelled John Galliano, from his stints at Christian Dior and Givenchy.

Some houses have responded by recreating their past hits, as with Dolce & Gabbana’s and Prada’s Re-Edition collections, marked with circa-dated labels, or by refashioning deadstock or spinning fabric from waste (Bode, Reformation, Prada Re-Nylon) and making sustainability a priority, as in making items that don’t threaten to quickly go out of style after going viral.

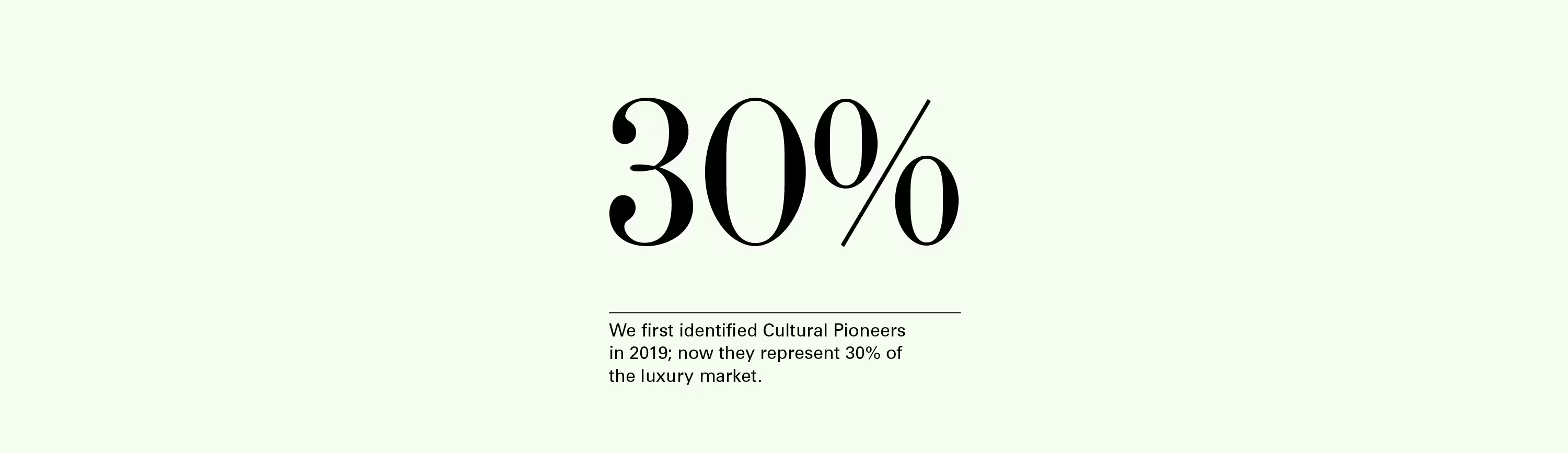

In 2019, we named a selection of respondents and interview subjects Cultural Pioneers, based on their behaviors pertaining to fashion. This sect is both authoritative and open to exploration, with higher purchasing frequency and often with jobs in creative/entrepreneurial fields. They skew younger and are more excited by fresh ideas from budding brands.

This year, through a series of pointed questions, we recognized a whole 30% of Core Luxury Consumers as Cultural Pioneers, which tells us that the cutting edge is expanding. As time progresses and access to information becomes more readily available, audiences are increasingly self-educating, seeing value in becoming an influencer’s influence rather than the influenced.

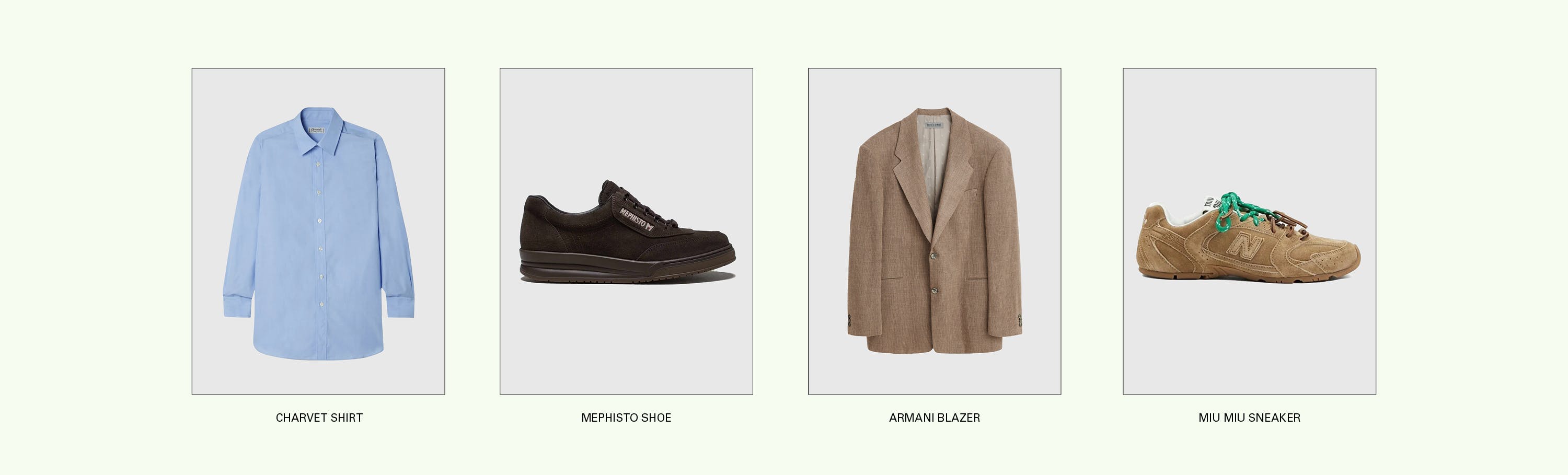

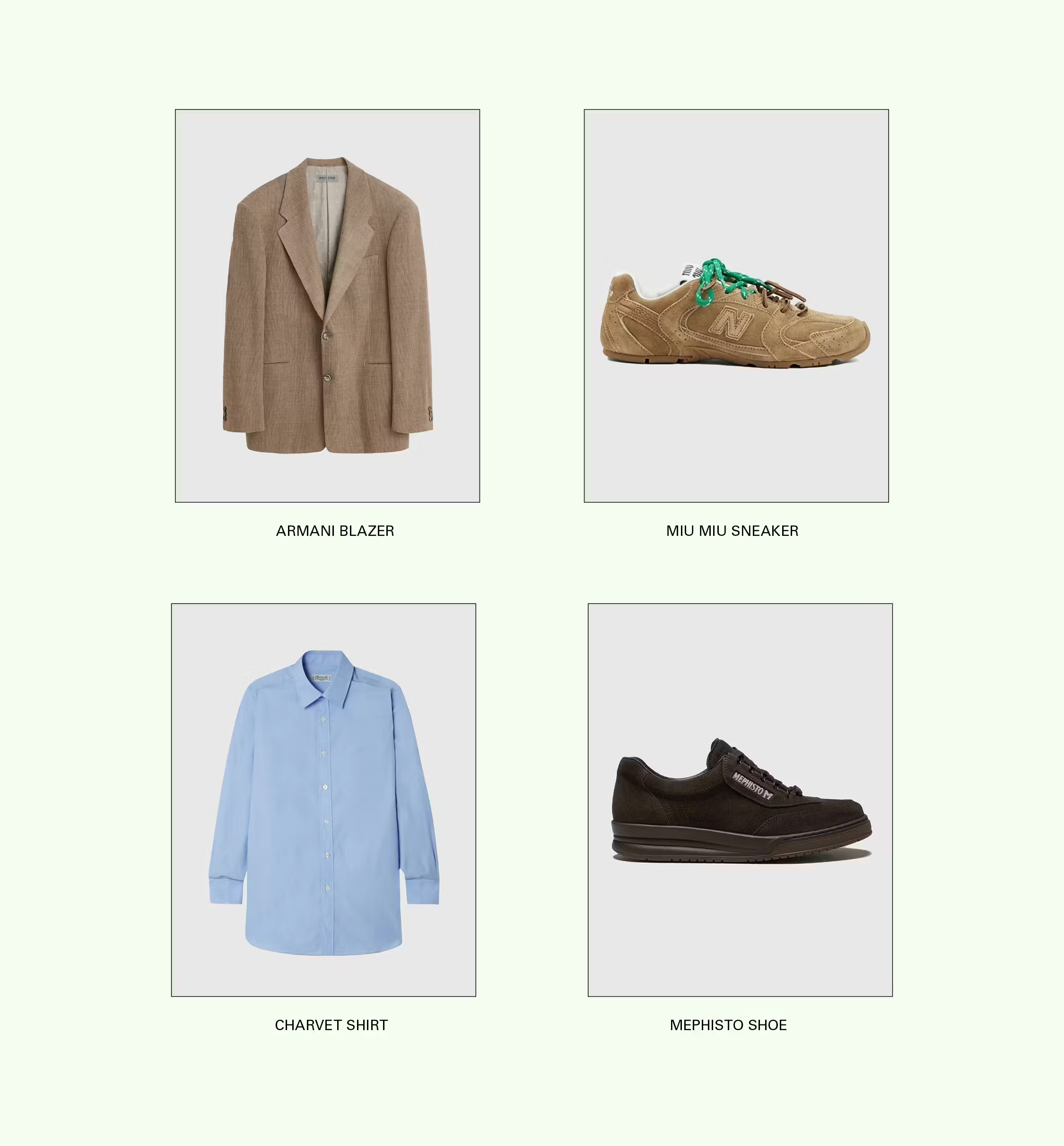

With this rise in consumer awareness, we see a rejection of gimmick and an emphasis on materiality when we look at last year’s top-trending products – High Sport cotton pleated pants; the adidas 1949 Samba; Schott and Carhartt and Barbour jackets; The Row jelly flats – and the must-have items of now – a tailored shirt by Charvet; an archival Armani blazer; monochrome Mephisto or Miu Miu sneakers. Each is basically unbranded, therefore easily duped, and so identity is mostly recognized through structural quality.

Decades-old design houses with aspirations of cozy nonchalance like Hermès, Brunello Cucinelli, Ralph Lauren, and Loro Piana are reportedly bucking downward trends, while the soft, layered separates and stoic marketing of Lemaire and the Olsen twins are oft-cited as inspiration for influencers and other working designers. Collections from the younger Toteme and Khaite clearly follow in these gentle footsteps, making big strides, each surpassing $100 million in 2023 sales according to the Financial Times and The Business of Fashion, respectively.

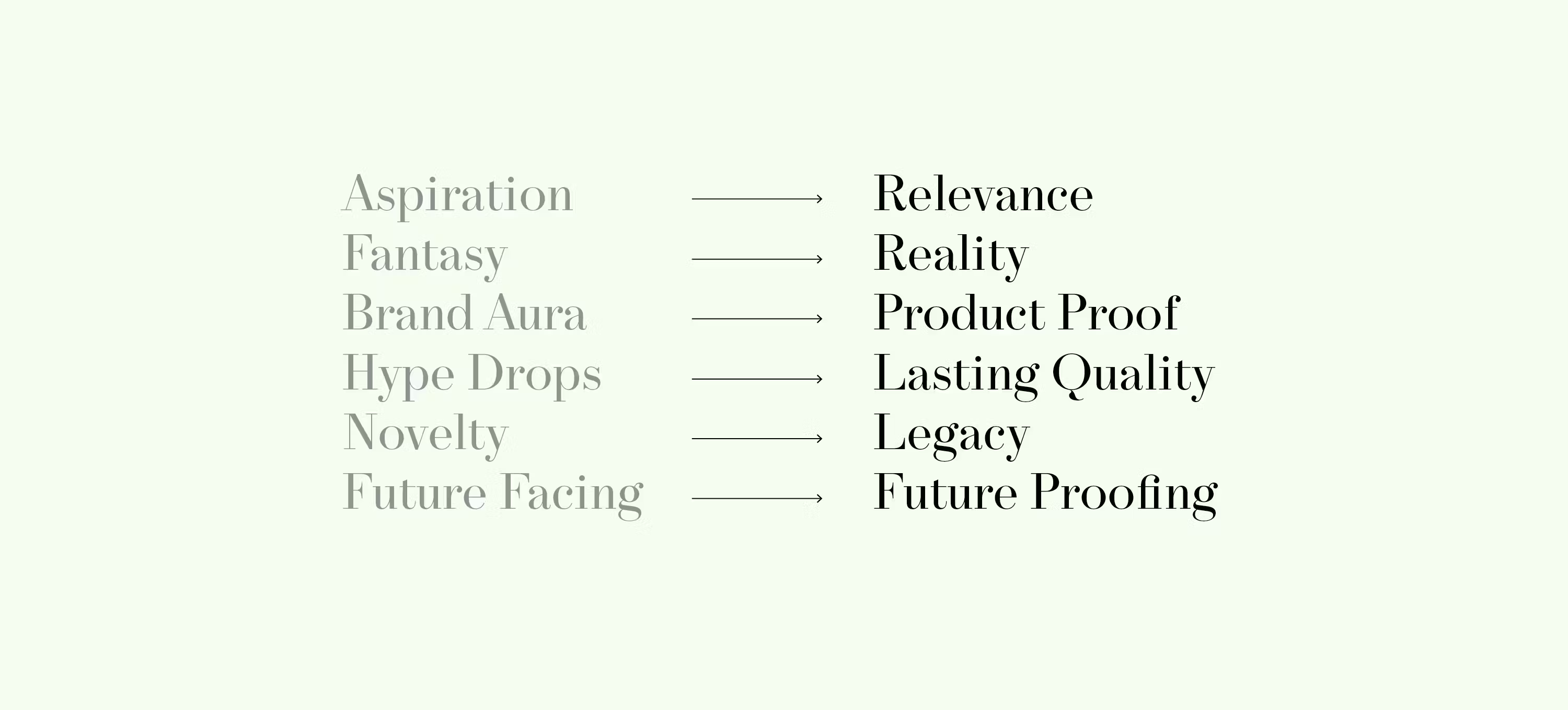

We might call this aesthetic Redefined Luxury: straightforwardness as a qualitative signifier due to its inherent transparency. Material superiority is made unmistakable with clean execution and no frills to hide it.

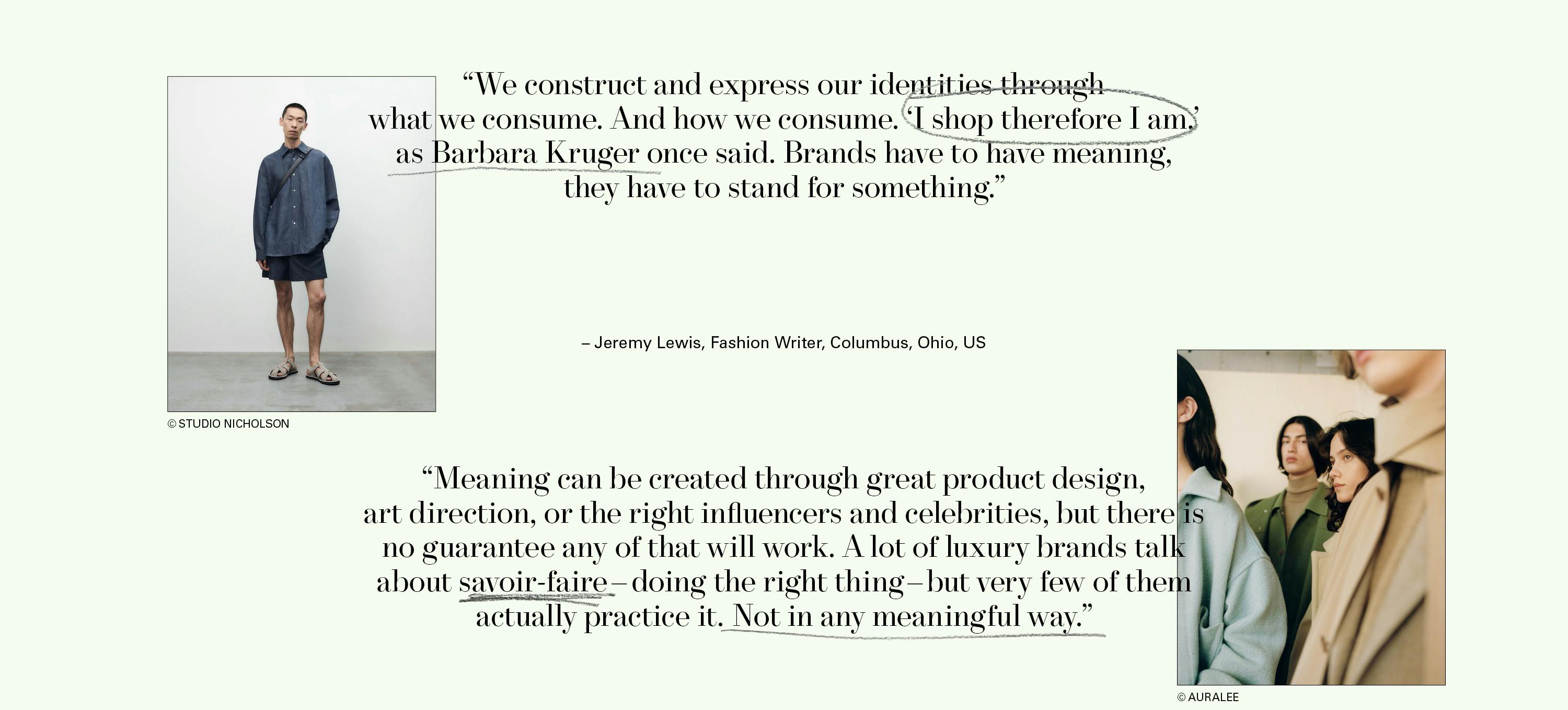

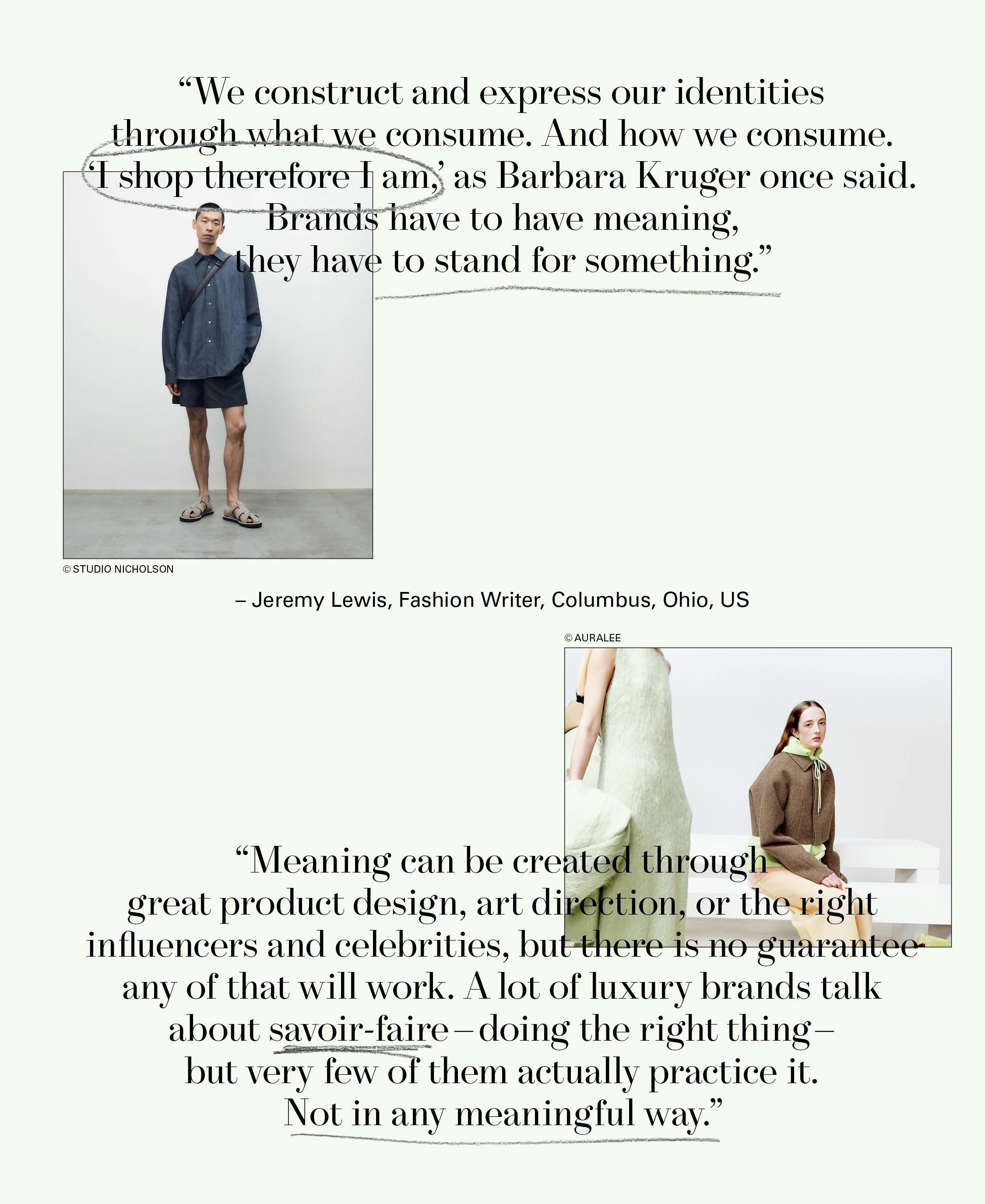

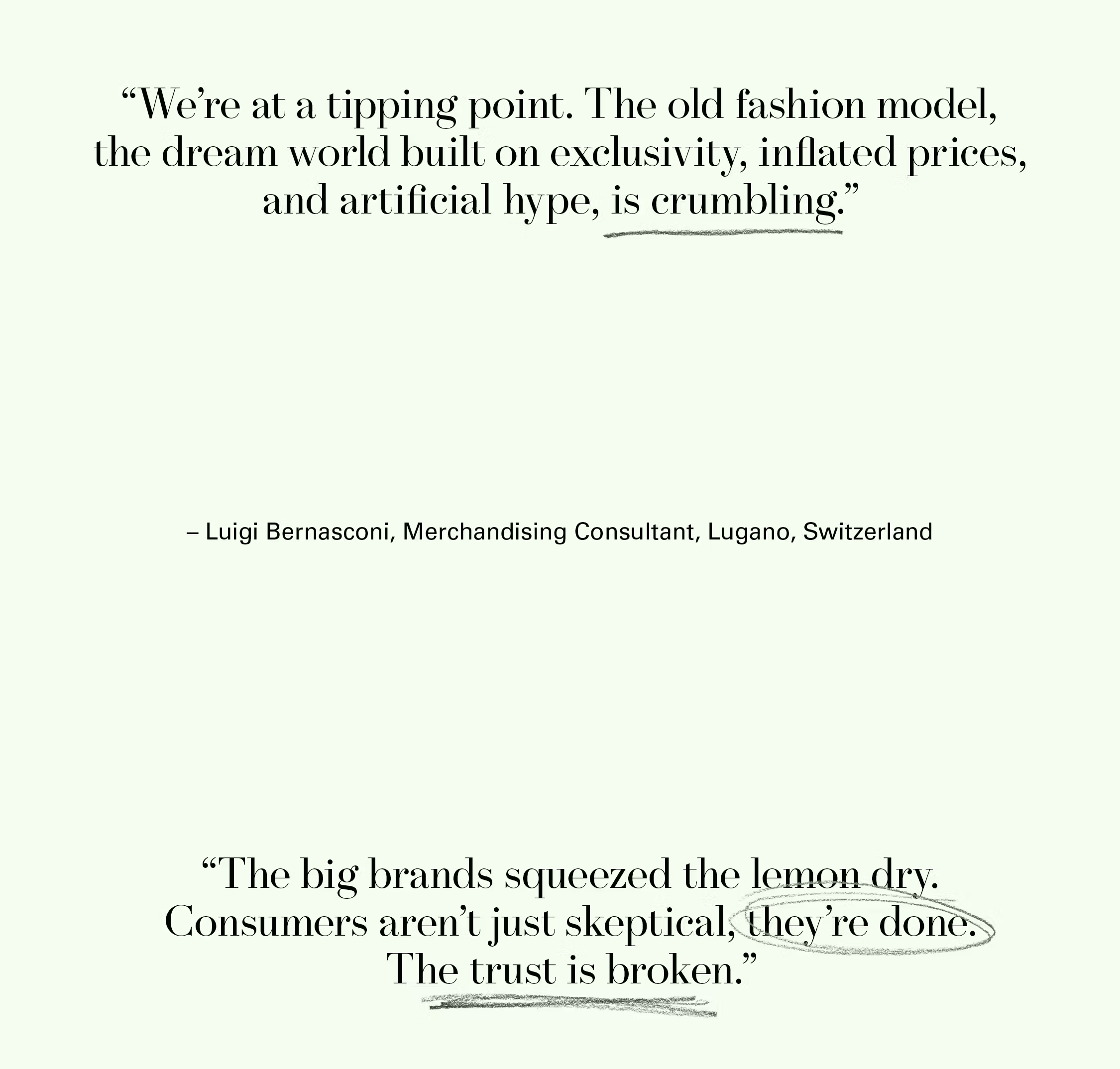

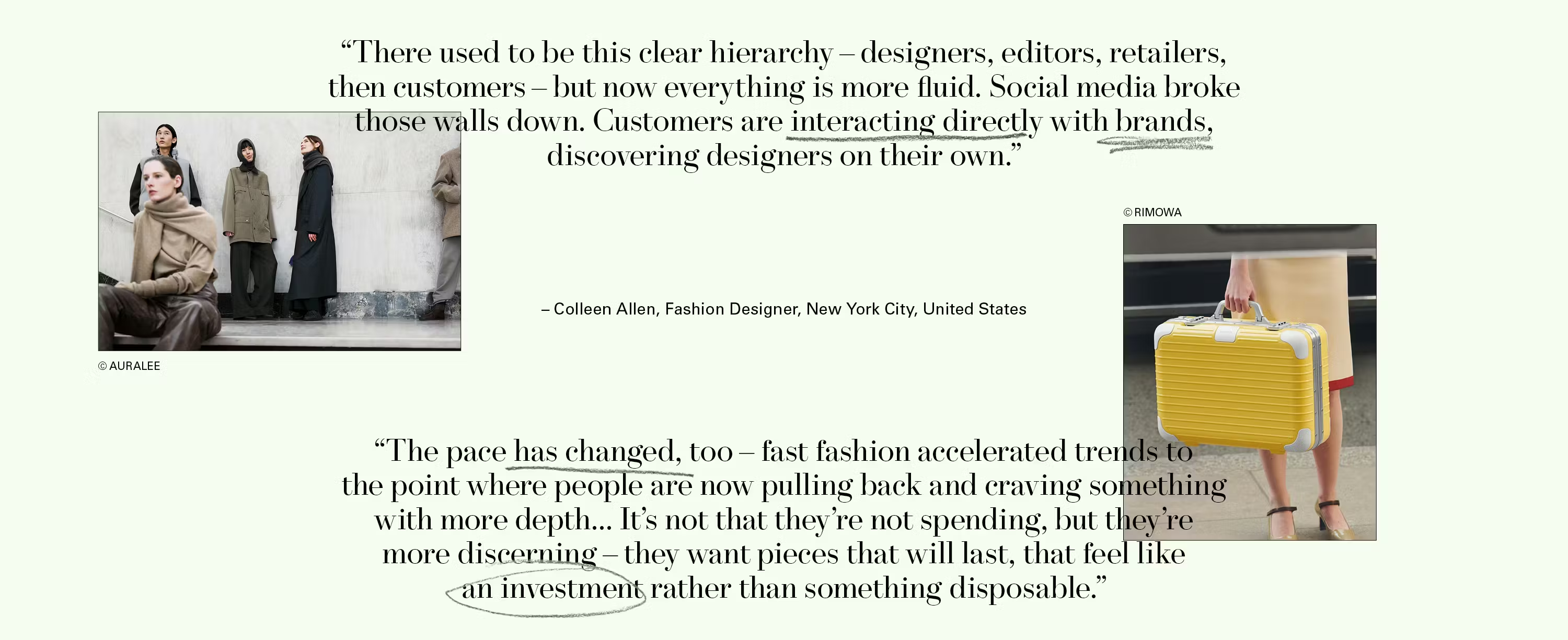

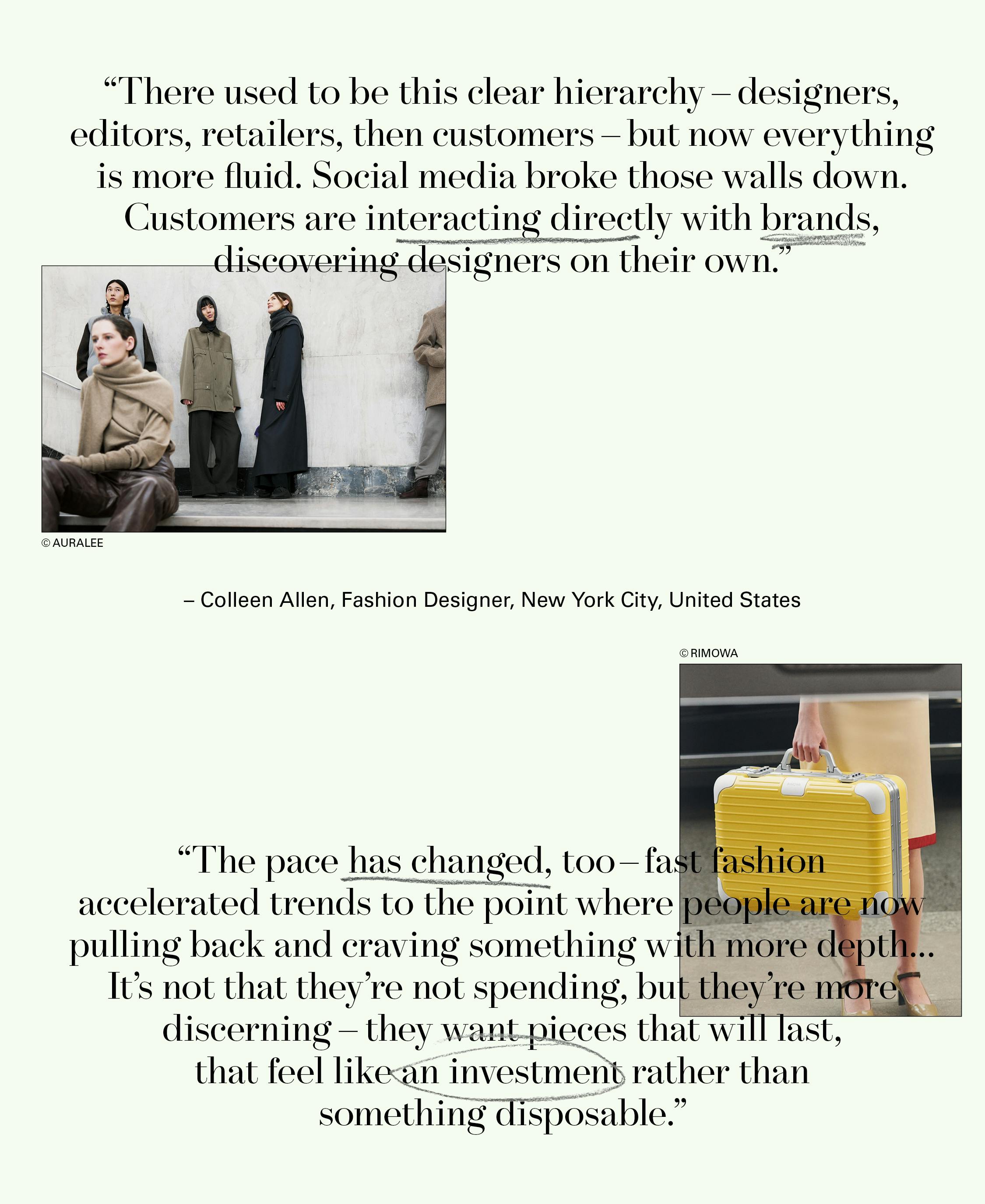

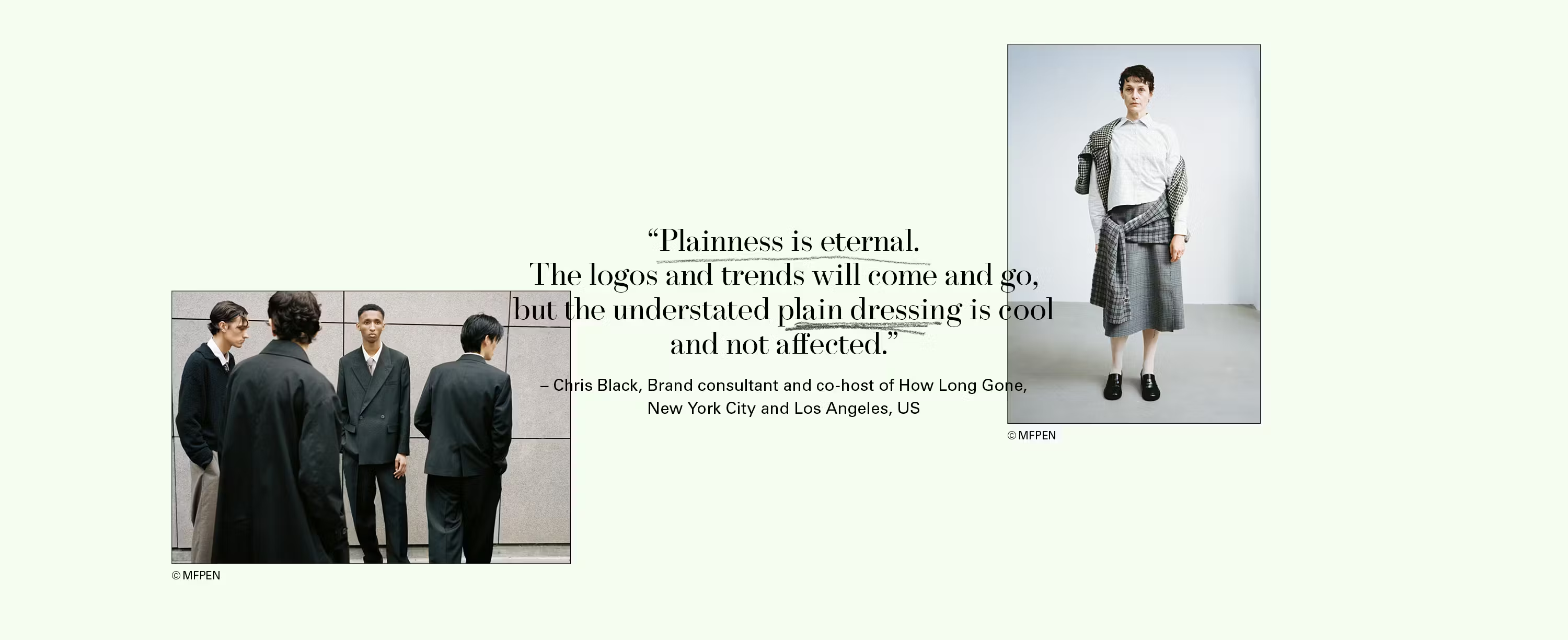

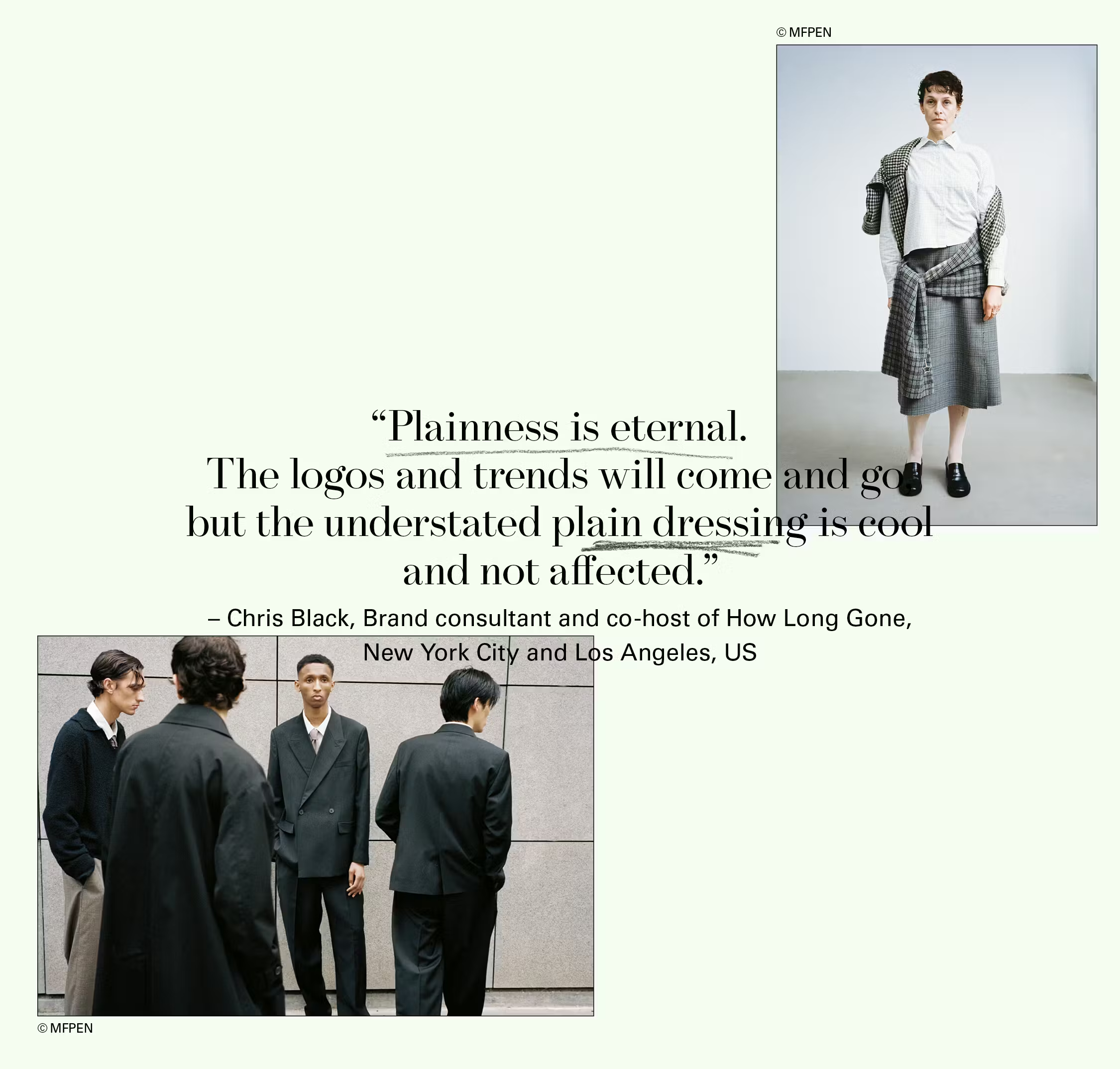

“For years, we were sold an illusion: that price was justified by craftsmanship, creativity, and heritage. But as transparency seeped in, it became obvious what we were really paying for was an aura, a constructed mystique, a marketing machine that ran out of fuel.” —Luigi Bernasconi

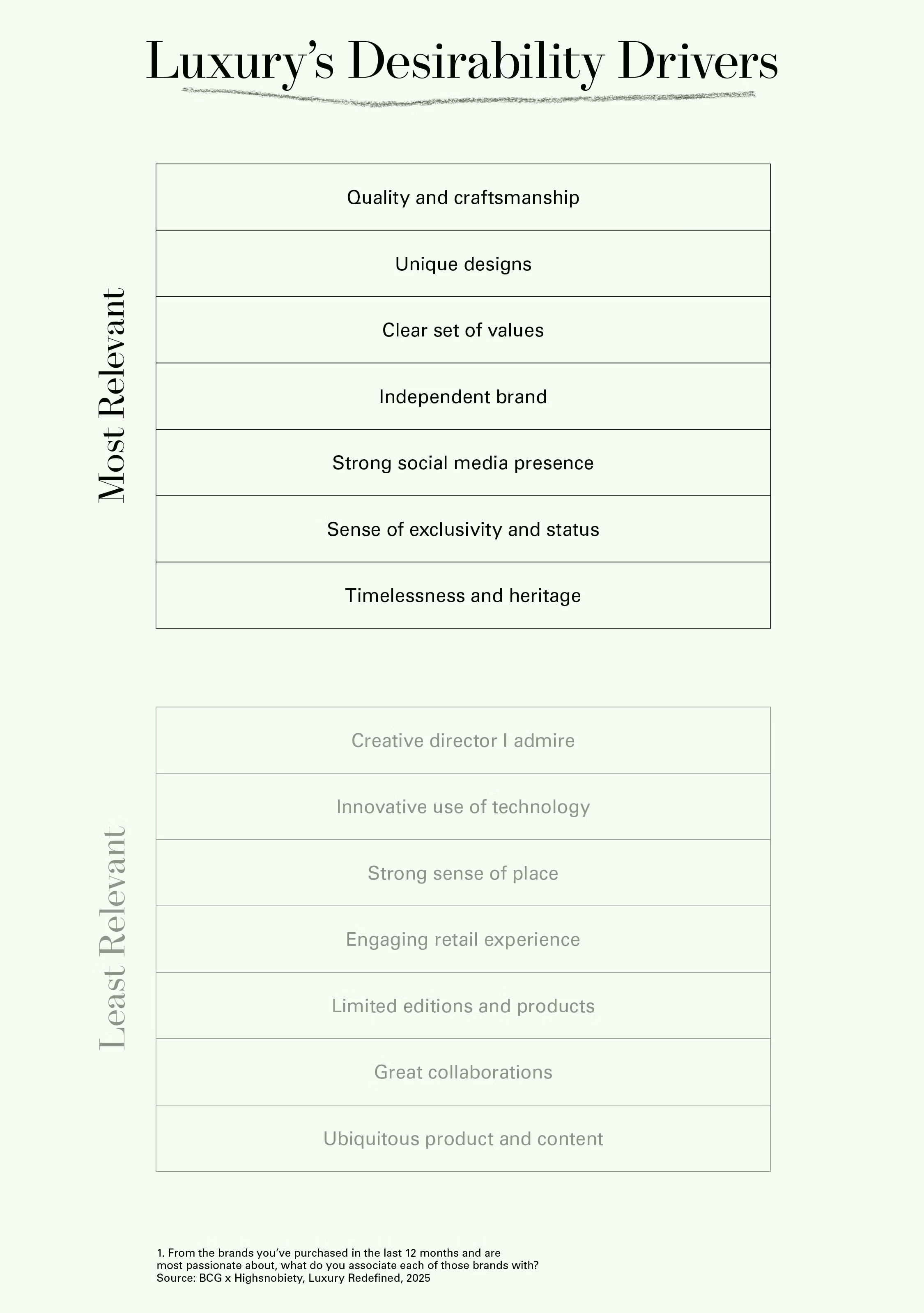

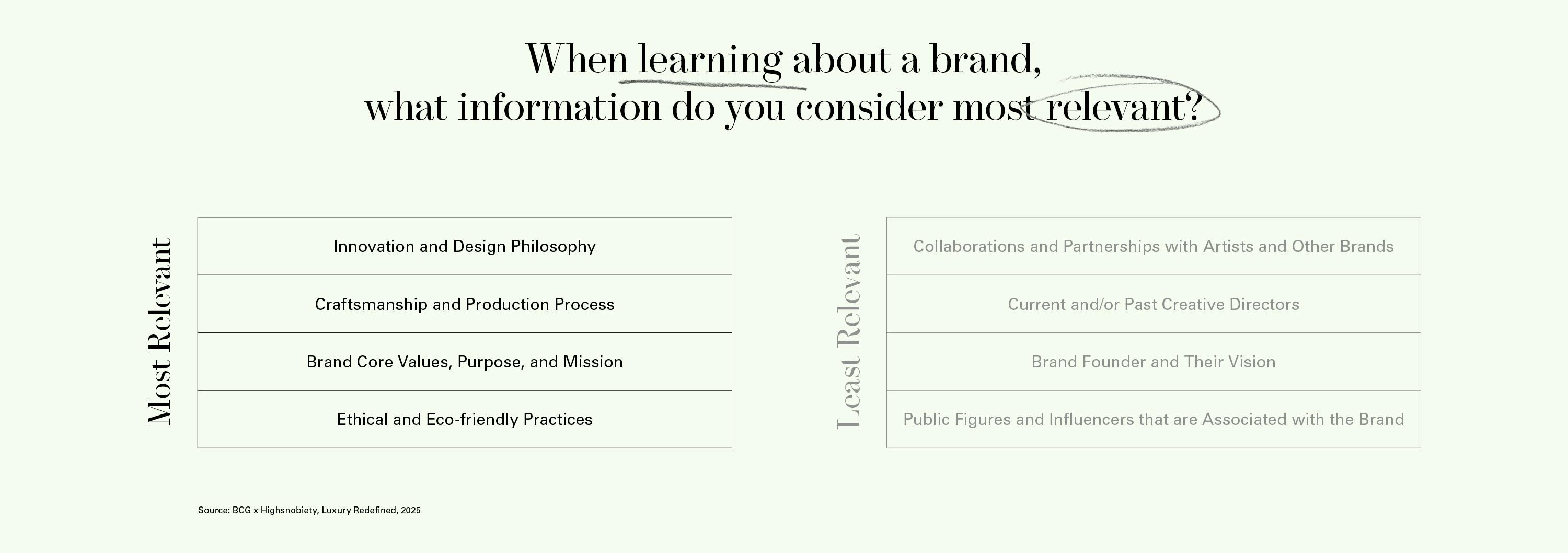

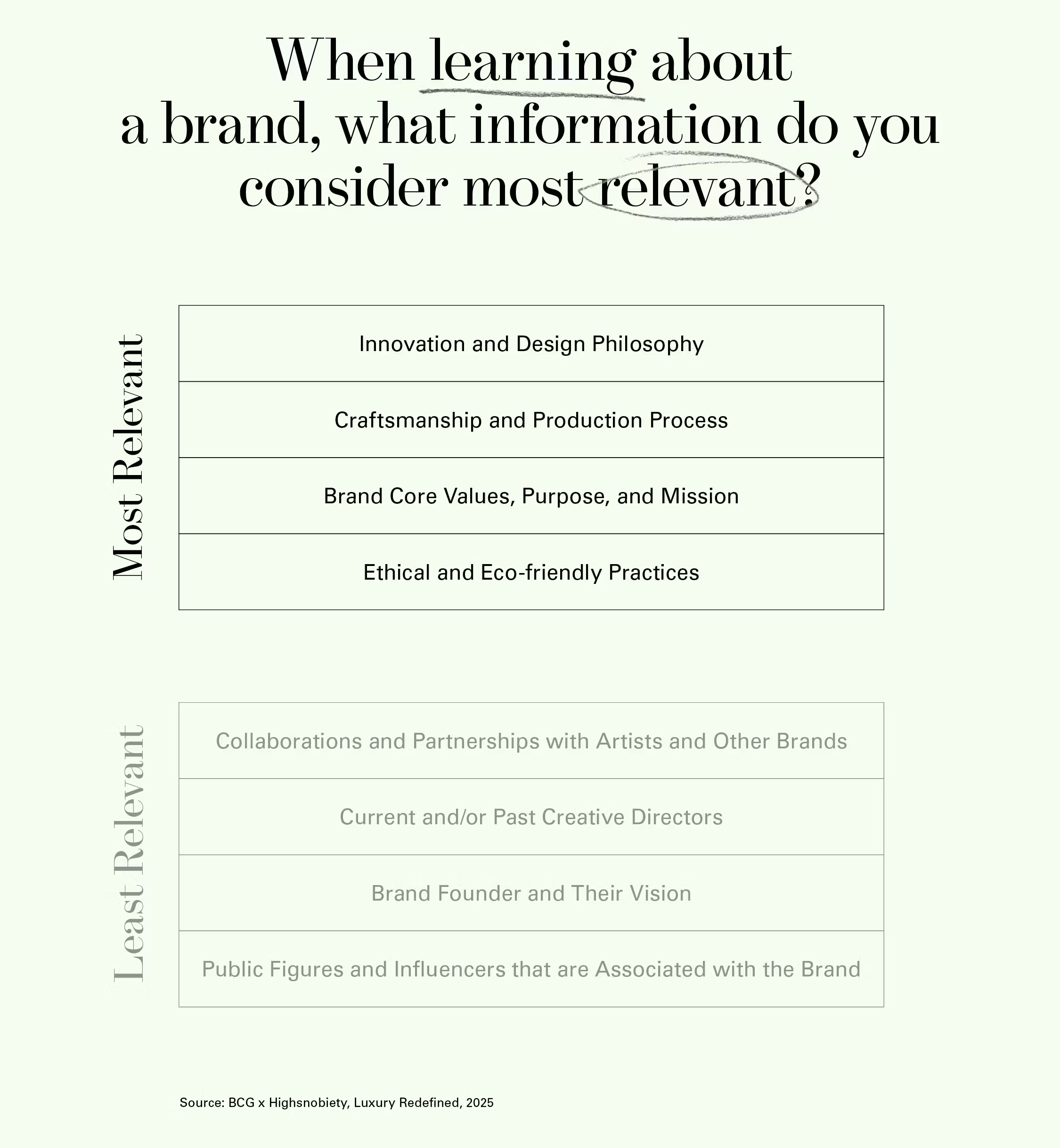

Luxury is still in demand, if in a different way. The top drivers of desirability for today’s luxury consumer – craftsmanship, uniqueness, clear values, and independence – are all related to the quality and the story behind a brand or product, not the marketing of it. Factors that are low on the list include collaborations, creative directors, and associated influencers – things that drive hype and engagement but not meaningful connection.

“Despite the ever-increasing push for commercialization, there are always bright spots of independence. Fashion is, at its core, a creative industry, and I believe originality and dynamic voices will continue to break through.” —Jesse Hudnutt, Fashion Consultant, New York City, USA

Brands once considered basics labels have broken into a new sphere of styling, their plainness now earning them credibility.

Designs consistently pinned by our Cultural Pioneer and industry expert interviewees as successfully answering to their own desires come from Auralee, Mfpen, and A.Presse, who take cues from Japanese, American, or Scandinavian workwear: blank linen aprons and double-reinforced uniforms; a parka that both weather-protects and elegantly slopes off the shoulder.

It seems that every luxury giant has shown their version of a slouchy leather bag, a crisp denim chore coat, and preppy staples such as loafers, polos, and sweater sets. Redefined Luxury is even more apparent with emergent, independent designers who make considered, not-cheap, small batches of the so-called essentials.

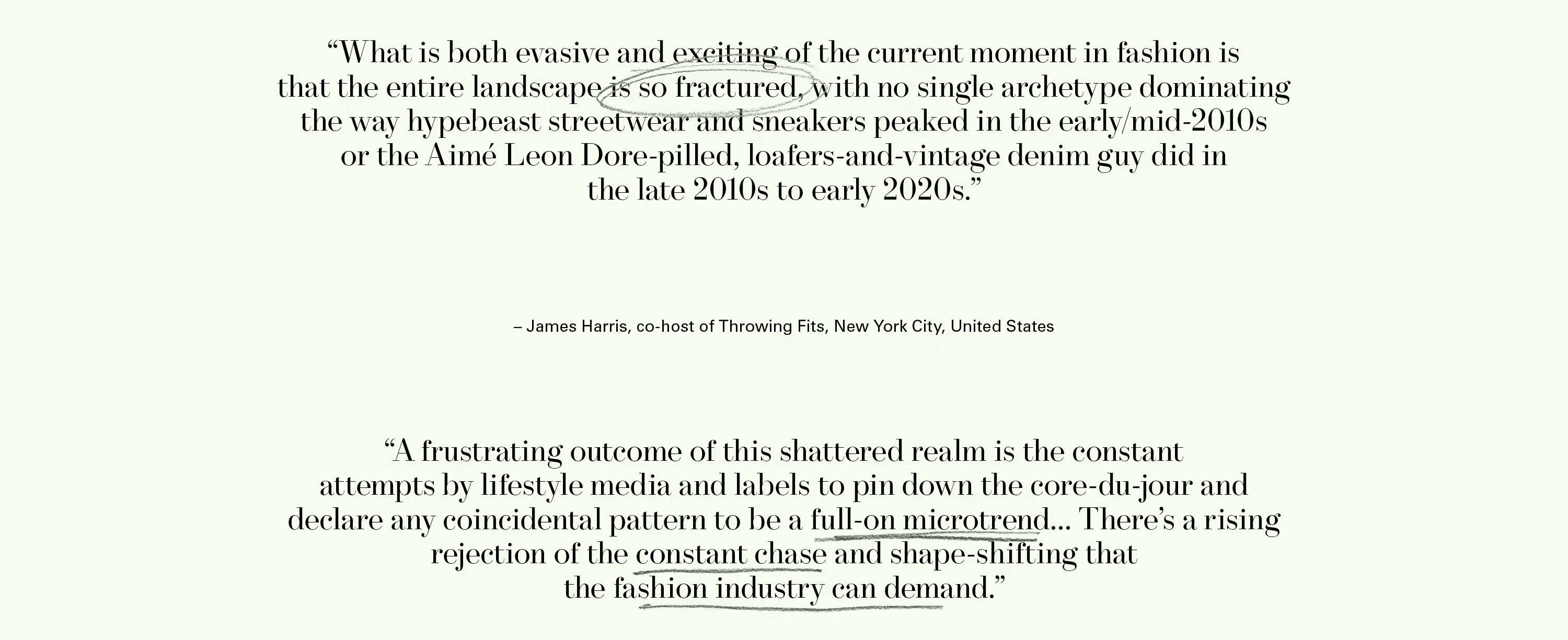

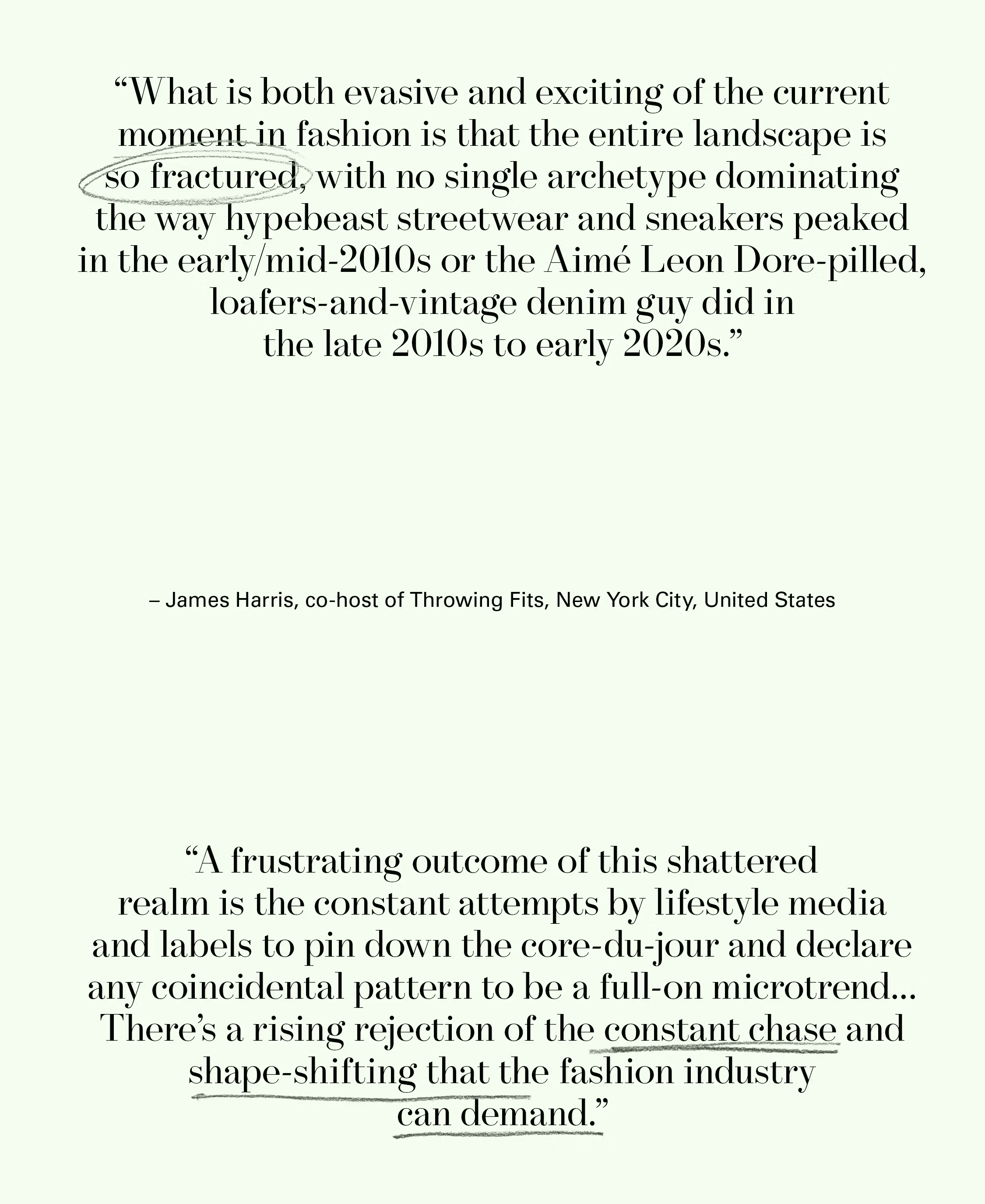

Judging from high fashion’s as-of-late heavy lean on the nondescript look, it may appear we’ve simply tired of cacophonous self-expression, that we’re returning to some status quo. But this pendulum swing away from noisy logomania feels further out than previous ones. We’ve weathered Elevated Grunge, Anti-fashion, Streetwear, Millennial Branding, Normcore, New Sincerity, Quiet Luxury/Stealth Wealth — each a reaction to a more ostentatious trend, and all of which, looking back, appear to be just that: a reaction, or palate cleanse.

Is what we’re seeing now simply more of the same, or is there, upon closer inspection, a distinction between typical fashion see-sawing and today’s offer from the leading millennial-led clothing companies? Based on responses from some of luxury fashion’s key players and clients, a significant set are fed up with the back-and-forth, preferring brands that take the risk of consistency.

And this aligns with the fashion reckoning we predicted half a decade ago. That a large portion of 2024’s Core Luxury Consumer group can be identified as a Cultural Pioneer tells us that our target demographic is, while investing in the brands that treat them as such, growing more culturally credible in their own right and rejecting trends that give off desperation.

Within the fashion set, talk of a designer replacement is often met with groans. Among all the faces associated with a brand, a creative director’s contract easily won’t outlast that of a young ambassador.

“Designer musical chairs seem to be moving much faster than ever before. You have to perform or you are out — and prices go up every season.” —Chris Black

That the designers of clothing are now seen as not much (if at all) more influential than wearers speaks volumes.

With the sped-up cycling of appointments, when there’s hardly time to put a face to a name, it’s difficult to stay inspired by one or another designer or house — giving independently-run brands the lead in straightforward storytelling.

When everything is available, the archive is right there, the bottom line needs meeting, everyone's an influencer, and in-person is optional, how do working designers respond?

Among the long-running high fashion brands doing exceptionally well today is Miu Miu – an especially interesting success story due to its being considered a sub-brand of parent company the Prada Group. Miu Miu had a reportedly impressive year in terms of growth and credibility, boasting record sales and showing up everywhere, from elite circles to social media virality (remember the Miu Miu Set?).

Not since its 1990s debut has designer Miuccia Prada’s pet project been so popular, and now as a womenswear brand readily adapted by all genders. As New York Times journalist Max Berlinger wrote in July 2024, “While Miu Miu officially trades in women’s clothes, its most recent surge in popularity is due, more specifically, to the men.”

There is something inherently wholesome about this brand’s winning year, even if it has only gone from big to bigger: There are well over 100 Miu Miu stores worldwide, stocking an ongoing collaboration with New Balance, recognizable fragrance bottles, best-selling matelassé leather bags, collections that close out official Paris Fashion Week, and advertisements featuring A-list stars such as Sydney Sweeney and Emma Corrin, lensed by top-billed creative teams.

Still, Miu Miu has maintained a humbleness of expression, perhaps particularly in relation to its parent. Unlike Prada, the collections of which are now co-directed by Raf Simons (no stranger to fashion’s revolving door, having helmed the houses of Jil Sander, Christian Dior, and Calvin Klein in the span of two decades), it has maintained the same creative head, Miuccia Prada, since its inception — going on 33 years.

The Miu Miu logo — a stenciled or stamped double row of semi-loops that denotes a certain naiveté, based on a childhood nickname of the founder — is sometimes prominent, but less so than Prada’s triangle mark, which started as a delicate plaque and now literally shapes the products, from diamond studs to perfume flasks.

Prada was founded as a travel goods store in 1913 by Mario Prada and was taken over in 1978 by his granddaughter. Miuccia brought with her a paradigm shift by introducing the idea of coveted Italian bags in industrial nylon as opposed to leather. In the late 1980s, Mrs. Prada designed her first ready-to-wear, and in the early 1990s, she branched out into menswear, the technically-focused Prada Sport line, and Miu Miu. She’s now one of the wealthiest women on the planet, with art museums, cafés, a yachting team, and hundreds of stores under her name.

The brands’ eyewear is licensed by the über-conglomerate Luxottica, their fragrance and beauty products by L’Oréal. Prada famously collaborates with artists, actors, architects, authors, influencers, and landmarks, throwing large-scale events outside of runway shows to solidify an intellectual yet partying ecosphere. Miu Miu, specifically, produces a celebrated short film series with the day’s top and upcoming female movie directors.

If Miu Miu doesn’t exactly fit the narrative of consumers’ turn toward a more soft-spoken approach, it does offer an answer to the type of cultural credibility a bigger brand can prove.

Luxury shoppers want to buy heroes at any price, high or low. Does personal style still exist? Obviously, but the term’s meaning might change when anyone’s tastes are monetizable.

With the opportunities that come from blogging, vlogging, podcasting, and image-making, just about everyone knows the potential of self-promotion.

Social media representation is today’s business card. With a rising necessity for personal branding in every field, consumers are more aware of business strategy than ever before. Those who were once enamored with the logo and its legacy are developing their own typesets and marks, therefore seeing how the marketing sausage is made. As so much of luxury fashion is based on the power of its branding, the reveal of that process is dangerous for the top tier.

Self-awareness, the absence of anything too cloying, and a straightforward approach to sales seem to be going a long way — remember the 1960s acronymic design principle: Keep it simple, stupid. The recent success of humble teams with consistent identities, smaller, expert curations at boutiques and consignment stores (alongside books and artifacts that tell the assumed customer about the person behind it all), and collections not governed by the fashion calendar speak to a turn toward farmer’s market mentality in the clothing space. There is a sense, among these smaller purveyors, of offering only the hand-crafted, the well-cared for, and the perfectly ripe.

We are seeing an upswing in hero-product businesses (think: On Running, High Sport, Starface) that focus on one item at a time, giving a sense of scientific understanding. In tandem, the larger ready-to-wear labels with vast offers are showing certain reverence to their own hero products (Louis Vuitton’s monogram luggage, Gucci’s horsebit loafers, the Hermès Birkin, adidas tracksuiting, Balenciaga’s Le City Bag, Bottega Veneta’s intrecciato, etc.).

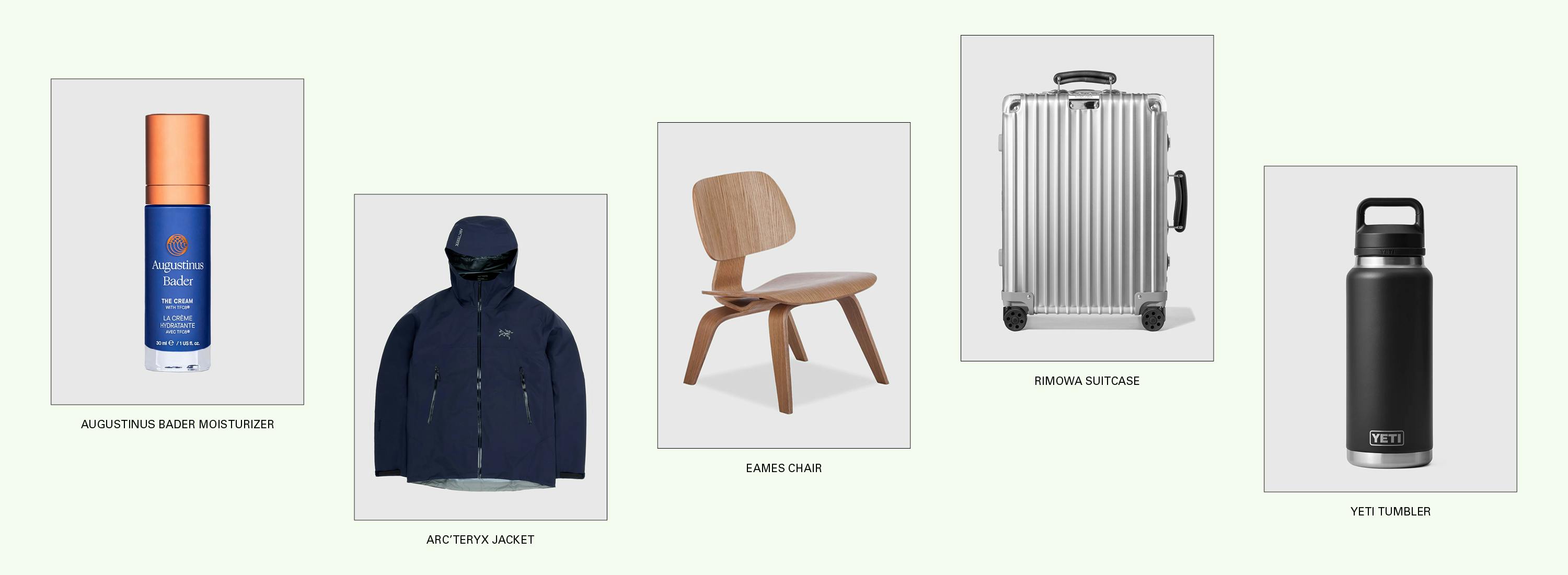

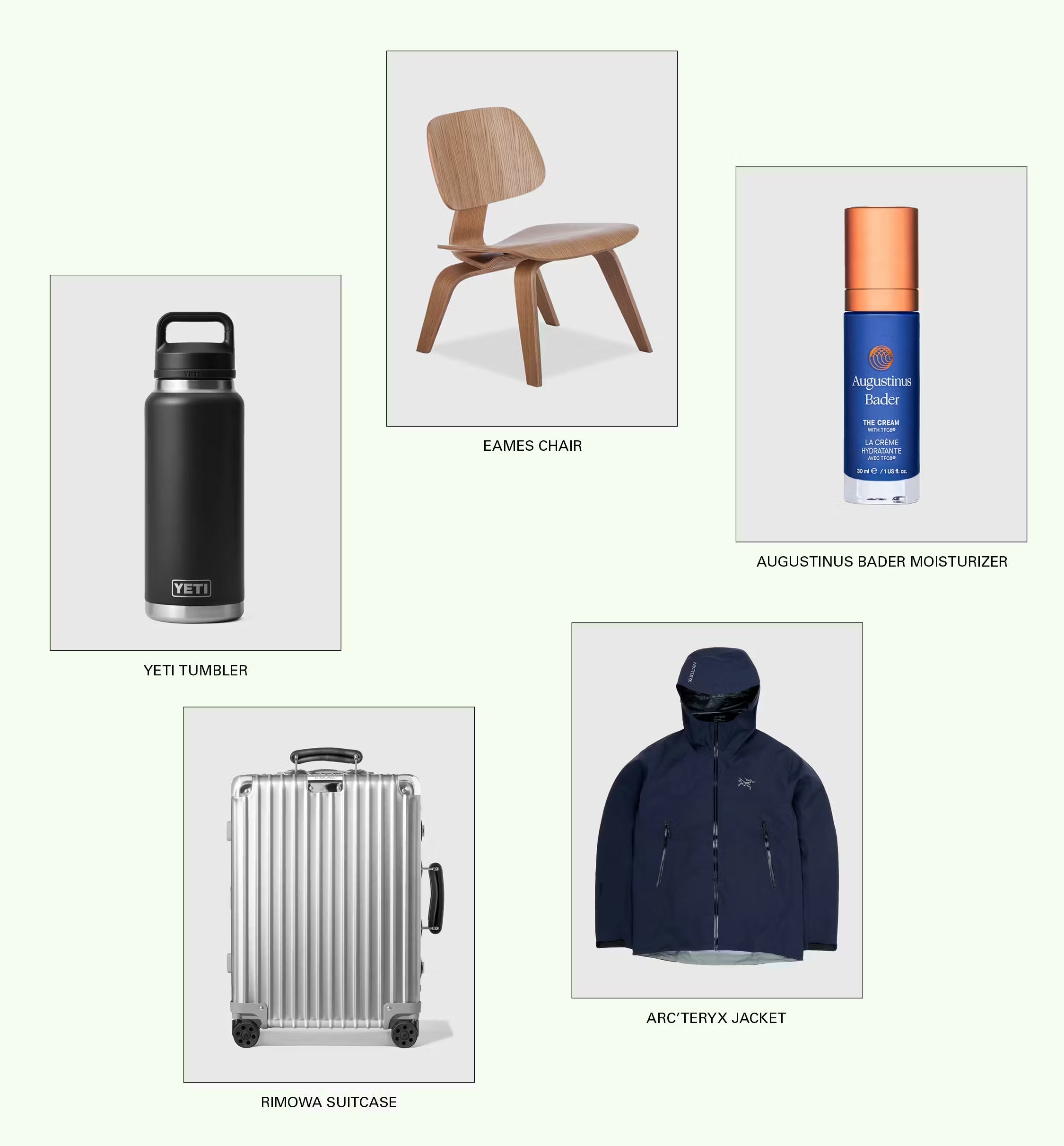

This coalesces with the doctrines of authenticity: designing what one knows, time-honored processes, ideas that get better with age. This isn’t a big box store, where one finds every little thing made in the same factory. Smarter consumers, now used to endless reviews that will eventually expose inferior products, want the one thing that each business makes best: CeraVe or Augustinus Bader moisturizer. An iPhone and a Mac. Arc’teryx or Patagonia weather protection. A Yeti or Stanley lidded tumbler. Rimowa rolling suitcases. Eames chairs. Maybelline mascara. A Louis Vuitton trunk. A Fendi fur.

We are living in an era of hyper-specific marketing that paradoxically aims to assimilate us. But with as many niches as we’ve created, monopolizing is impossible and trends are more difficult to track — signaling a revival of style over fashion.

This is both good and bad news for creative directors, who are improbably tasked with simultaneously pleasing the edge and the center — the local Cultural Pioneer and the mass global consumer. The less achievable this becomes, the more apparent the paradox.

Challenges deepen when providing for everyone, with multiple collections per season, eventually means pleasing no one. The pressure to make larger profits, compete with dissimilar brands, and answer to broadly mined data and irrelevant consumer trends inevitably distracts and waters down ideas. Eventually, more attention is paid to one-size-fits-all departments and to remaking best-sellers as opposed to experimentation.

Meanwhile, smaller brands are allowed more agility and a return to respecting personal style is proliferating in boutiques and on our feeds. Luxury consumers want individual pieces that fit into their own concepts and cultures, not one big impenetrable picture. This shift is illustrated with craft tradition, a dearth of large logo marks, an indie resurgence, and attention to sumptuous detail.

“This shift isn’t just about fatigue; it’s about a fundamental recalibration. People now want clothes with depth, soul, and identity. Something that resonates rather than dictates. The new paradigm isn’t about owning the latest, but about curating pieces that last… Consumers have more tools than ever to judge what’s worth their money. They see through the greenwashing, the forced narratives, the desperate attempts to stay relevant. I…In this reset, the brands that will thrive are the ones that stand for something beyond hype. Those that create with intention, with authenticity, with a deep respect for their customer’s intelligence.” — Luigi Bernasconi

Luxury fashion is being reclaimed by consumers who are savvier, more intentional, and less excited by hype. The brands that will define the next era are not necessarily the loudest, largest, or even the most innovative, but the ones that listen best – those who trade spectacle for substance and status for storytelling. In a market saturated with sameness, authenticity is key. And rather than price dictating relevance, brands will be smart to rely instead on craft and cultural fluency.

Credits

Author: Natasha Stagg

Research & Insights in Collaboration with BCG: Flavia Gemignani & Yasmine Hamri

Senior Director, Global Research & Insights: Anna Burzlaff

Designer: Tetiana Khvorostiana

Copy Editor: Amirah Mercer

Publisher: David Fischer

Editor-in-Chief: Noah Johnson

SVP & General Manager HS+: Munise Can

VP Content & Activations: Matt Carter

Director, Editorial Operations: Jake Indiana

Brand Creative Director: Chloé Techoueyres

Senior Visual Editor: Manus Browne